Growing EV production will see higher prices for nickel and cobalt

Nickel28 is a lower risk long term potential income play

Nickel28 (NKL.TO) is a relatively new company once called Conic Metals that came into existence as a spin off from Cobalt27 at the time that company was taken private. It owns a carried interest in the massive Ramu nickel cobalt mine in Papua New Guinea and a portfolio of streaming royalty interests in development stage mining projects concentrated in nickel and cobalt but not yet producing. The company has 86 million shares outstanding which trade at about $1.00 per share in Canadian funds or about $0.78 per share U.S. Since the company reports its results in U.S. dollars I will use that currency throughout this article, and note that in U.S. funds Nickel28 has a market capitalization of less than $70 million.

Ramu Mine interest

The company is debt free at the parent company level but does have non-recourse debt associated with its carried interest in Ramu.

Non-recourse debt is an obligation that Nickel28 is not obliged to pay but is paid down from the company’s share of the cash flows of the Ramu mine. Nickel28’s share is a 8.56% carried interest and which at today’s nickel and cobalt prices provides the company with an approximately $30 million U.S. attributable cash flow. That cash flow should retire the non-recourse debt (which at June 20, 2021 stood at $94 million).

The Ramu debt has two forms - operating debt and construction debt. Cash flow is first applied to construction debt which at June 30, 2021 was $10.2 million. Nickel28 estimates the operating debt will be retired from Ramu cash flow before year end 2021. When that occurs, 35% of Nickel28’s share of attributable cash flow from Ramu is paid directly to the company while the balance is applied to the construction debt. That means that in 2022 Nickel28 should begin to receive approximately $10 million cash flow in its hands which can be used to pay corporate expenses, fund dividends or stock buybacks, or expand the portfolio of streaming interests. Corporate expenses have been running at an approximate $5 million annual rate.

Assuming nickel and cobalt prices remain more or less at today’s levels and the Ramu mine operates normally, the $84 million construction debt should be repaid within 4 years. From that time forward, Nickel28’s interest in the Ramu mine automatically rises to 11.3% and its pro rata share of Ramu cash flows are paid directly to Nickel28. By then, ignoring its streaming interests, Nickel28 should be a debt free company with cash flows north of $30 million per year net of corporate costs.

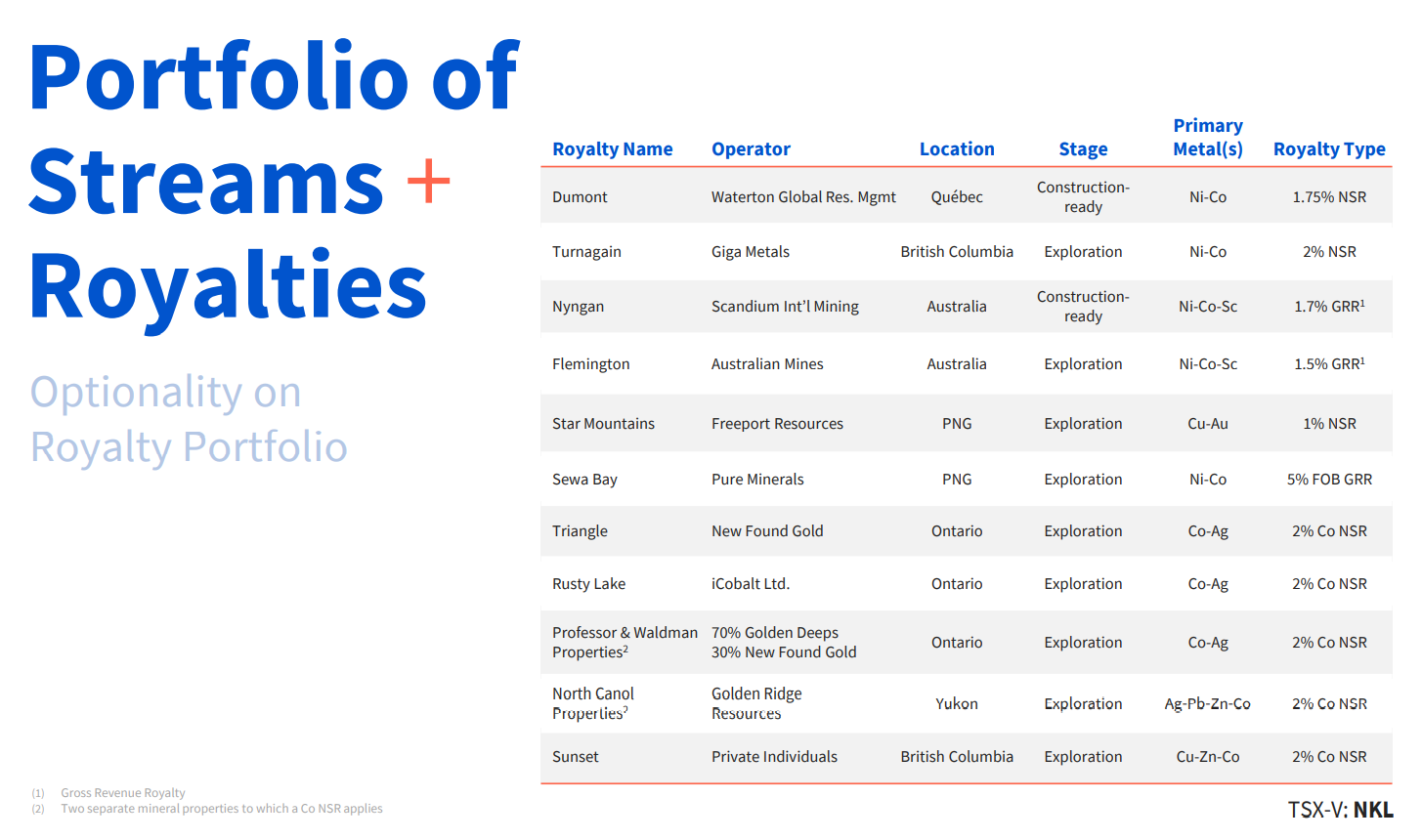

Streaming Royalty Interests

Nickel28’s portfolio of streaming royalty interests comprises Net Smelter Royalties (NSR) or Gross Revenue Royalties (GRR) on 11 mining projects.

Each of these assets is independent of one another and can be valued separately. For the purposes of this article, I have valued only the 1.75% NSR on the fully-permitted Dumont nickel project in Quebec, one of the world’s safest mining jurisdictions. Dumont is a world class deposit containing some 6 billion pounds of nickel according to the NI43-101 report on the project and is privately owned by Waterton Global Resource Management. That technical report contemplated annual production of 39,000 tonnes of nickel which over the planned 30 year life of the mine amounts to 2.5 billion pounds of recovered nickel. At today’s approximately $8 per pound nickel price, total nickel revenue of $20 billion results and a 1.75% NSR generates life of mine cash flow of ~$350 million paid to Nickel28.

No one can forecast commodity prices with any accuracy but there is a tailwind for nickel prices. Nickel is a key metal for battery production and the expected demand for electric vehicles (EV’s) is project to double nickel demand over the next decade. There are few sources to supply the added demand and there is a reasonable probability Dumont will be one of those sources.

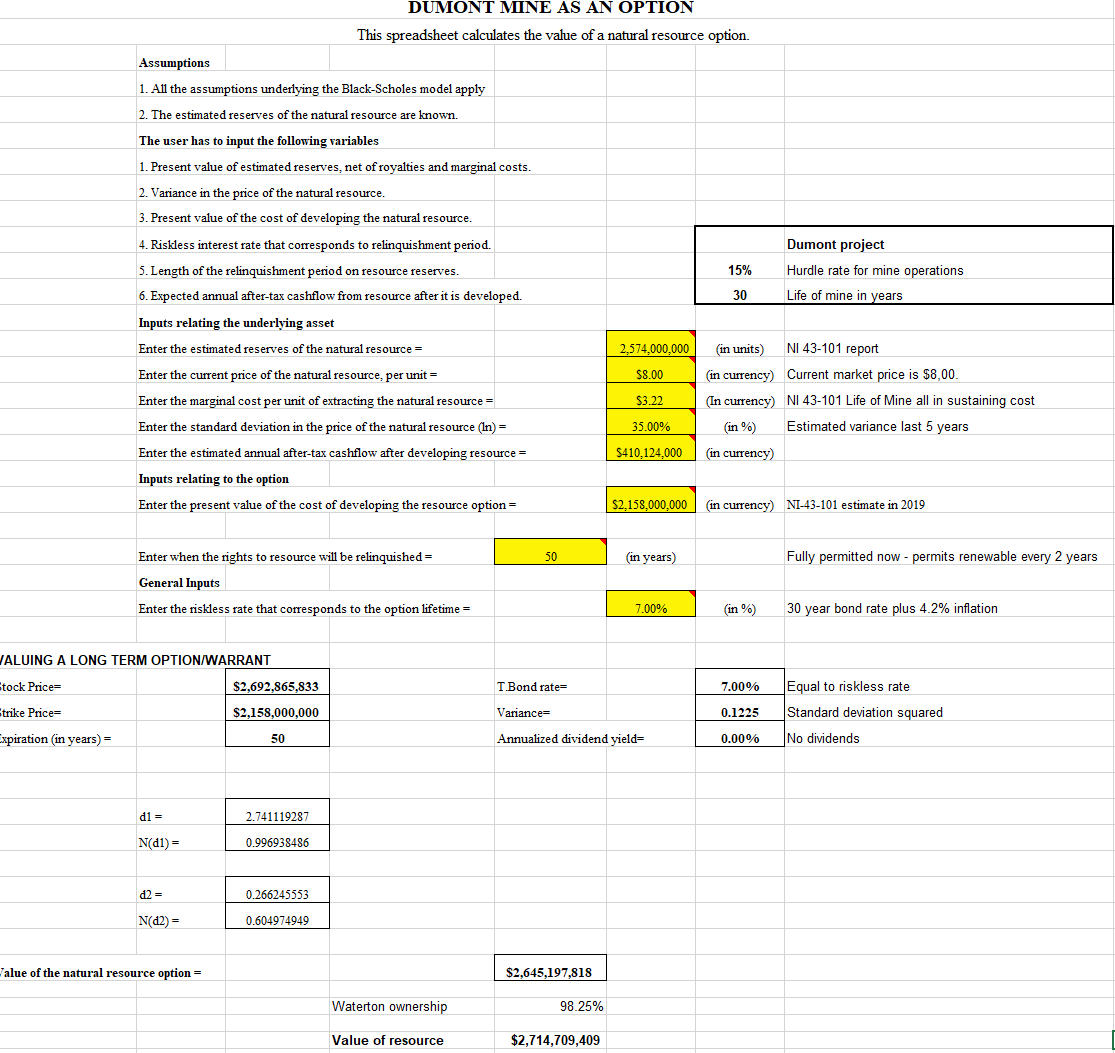

Modern valuation techniques value ore in the ground as a “real option” on future commodity prices and demand, and the Black Scholes option pricing method is a method which produces reliable valuation estimates subject to all the uncertainty that valuation of future cash flows contains.

Based on the NI43-101 data I have used Black Scholes to value Dumont at approximately $2.7 billion indicating that this fully-permitted mine is likely to benefit from a positive investment decision in the next few years barring a collapse in nickel prices.

Again, based on the assumed $8 per pound nickel price and project annual production of 39,000 tonnes of nickel per year (equivalent to 86 million pounds), Nickel28 should receive about $12 million annually for the 30 year mine life for a total of $360 million. Even with a positive investment decision that cash flow is at least 3 years away, and discounting $12 million annually for 30 years beginning a conservative 5 years out produces a value today of about $80 million. If nickel and cobalt prices increase under the pressure of EV demand, that value could be much higher.

Conclusion

Nickel28 is an undervalued, debt free stock offering investors long term exposure to nickel and cobalt which may benefit materially from the growing demand for EV’s. With low corporate costs the company can be reasonably expected to begin paying dividends once the Ramu non-recourse debt has been retired, if not sooner.