Gas inventories tell a troubling tale of woe for Democrats this winter

But low storage points to robust returns for producers and investors

To set the stage, consider natural gas storage in 2021.

On July 15, 2021 natural gas in storage was 3,623 Billion cubic feet (Bcf) in the United States and 696 Bcf in Canada. Four months later, on November 16, 2021, the first draw on storage took place and natural gas storage began filling the gap between production and consumption for the winter period. Those storage levels compared to 2,629 Bcf on July 15, 2021 in United States and 495 Bcf on the same date in Canada. In the four months between July 15 and November 16, 2021, production in excess of demand added 1,195 Bcf to storage levels.

Fast forward to 2022. Storage levels as of July 7, 2022 were 2,311 Bcf in America and 372 Bcf in Canada are 1,656 Bcf less than on July 15, 2021. This week an injection of 60 Bcf is projected. With only four months until the withdrawal season begins, North America has 1,596 Bcf less natural gas in storage to assist in supplying winter demand.

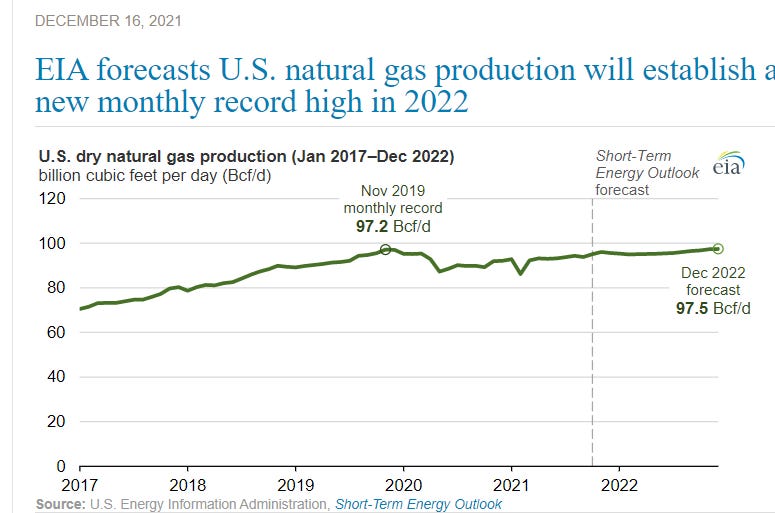

Last December the Energy Information Administration (EIA) projected U.S. natural gas production for 2022 would reach 97.5 Bcf/day. That has yet to happen with current week output flat at 95 Bcf/day.

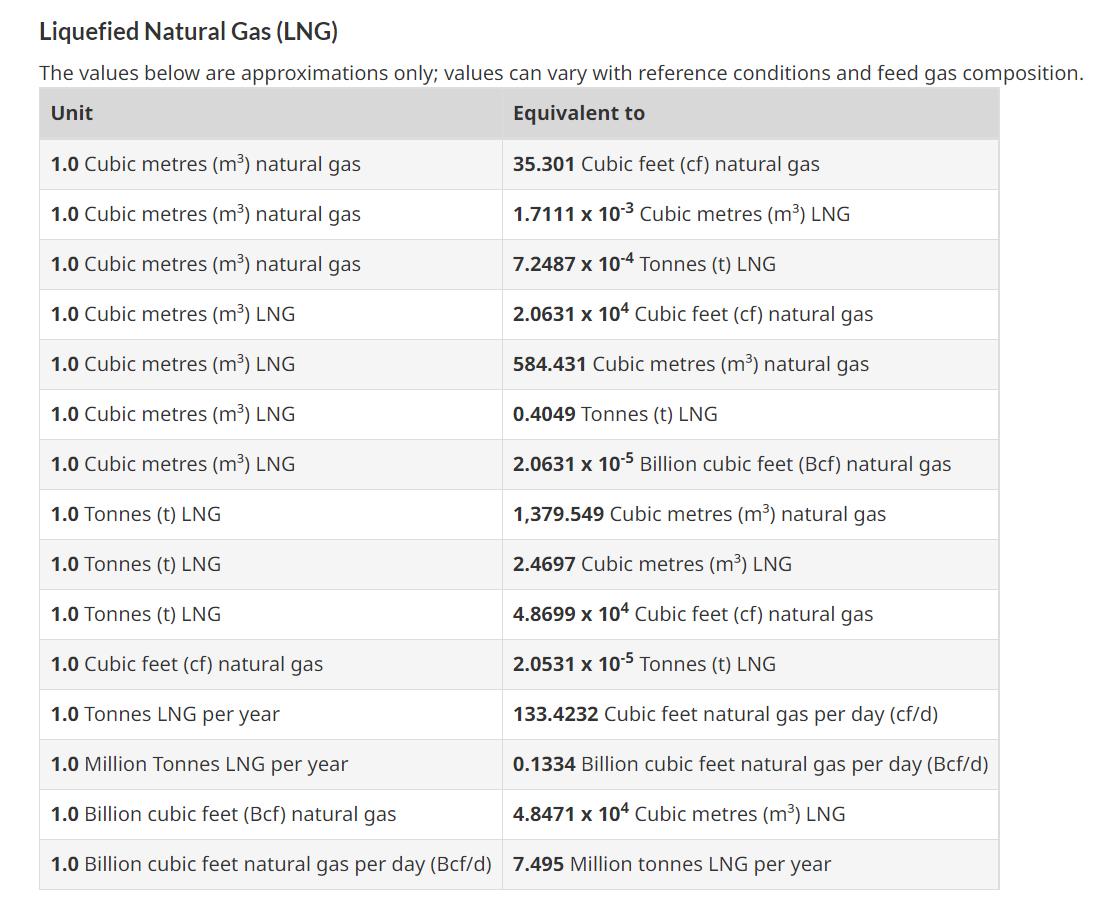

With just sixteen weeks to go until withdrawals begin, I project we will enter the withdrawal season with record low storage inventories. In parallel with the perilously low storage numbers, according to Forbes Magazine President Biden has committed to shipping 15 billion cubic tonnes of LNG to Europe this year and 50 billion cubic tonnes in 2023. Forbes’ reporting was wrong, no doubt confused by the units. Conversion of units can be confusing so here is the Canadian government conversion table for LNG.

CBS, reported the commitment was 15 billion cubic meters (bcm) in 2022 and increasing to 50 bcm by 2030. This report was accurate. Moreover, the commitment was not confined to U.S. shipments, but includes U.S. allies. Here is link to the fact sheet published by the Biden Administration March 25, 2022 when the deal was cut.

One billion cubic meters of natural gas is equal to 35.3 Bcf. Fifteen billion cubic meters this year is the equivalent of 15 x 35.3 = 530 Bcf or about 2 Bcf/day for the 9 months from March 31, 2022 to year end. 50 bcm by 2030 is 1,765 Bcf or ~5 Bcf/day.

The commitment numbers are manageable but put pressure on an already tight supply-demand balance in North America. The agreement includes unspecified allies which I suspect must mean Canada since I don’t know of many other “allies” who can materially add to natural gas output. United Arab Emirates could make a contribution if it were considered an “ally”.

Without a material rise in gas production, North American natural gas markets may import the European natural gas price disease where prices of US$30 per gigajoule or more are now common. Either Biden abandons his “climate activist” base and encourages more drilling, or America will have to choose between reneging on its commitment to Europe or suffering very high natural gas prices. With inflation reported at 9.1% in United States this morning and Democrats deluded by the “climate change” rhetoric, voters tolerance for either will be tested.

Biden’s commitment to Europe will not fill the supply gap Europe faces for gas, and we are already seeing Germany, Austria and France returning to coal-fired power to ease the pressure. European gas prices should remain very high. With American producers having an incentive to increase production to meet Europe’s needs, they will do just that but with the high prices in Europe, their incremental output will be sent to that market leaving United States market tight and effectively importing higher prices for domestic gas.

For interest, at US$30 per gigajoule, Birchliff Energy (BIR.TO) would have cash flows north of CAD$5 billion; Peyto (PEY.TO) would have cash flows of about CAD$8 billion and Tourmaline would have cash flow of ~CAD$40 billion. I don’t expect any of those numbers to materialize but I do expect to see very solid profits in Canadian natural gas stocks for the next few years.

I agree, that if the western world wants long term control over inflation, then you MUST have low cost energy, plenty of it & plenty of sources for it.

Sadly, left wing policies & the green agenda, have destroyed that prospect.

The situation is already getting serious in Europe, worse, Putin now has huge control over an entire continent.

Because of failed energy policy, there is no ability to readily switch. Russia has been reducing the flow of natural gas for some time - preventing the normal build for winter inventory.

The dry summer & lower Rhine means that alternatives like coal cannot be built up over summer. In Germany, the utilities are on the brink of insolvency - bailouts will be required + power cuts.

Spot price is so high - they are now DRAWING N.G. from inventory, rather than building - in the middle of JULY!

France is having various issues of its own with electricity generation - which will likely affect us in the UK???

Germans will not stand aside as their industries etc collapse - something has to give!

The entire continent is beginning to rise up and protest over rising costs / falling living standards / farmers protesting the policies of the WEF & loss of livelihoods.....

I'm afraid that the show-down with Russia has so far been lost - the EU will likely press for a surrender deal along with whatever message that sends to Russia & China for the future. It didn't have to be this way - unless Biden thinks there is a quick military solution at his fingertips?