Fixed income investing?

Stop klidding me, fixed income securities are losing propositions

By a wide margin, the fixed income market dwarfs the market for stocks. Governments borrow trillions, corporations borrow trillions, Wall Street packages up mortgages, credit card balances and car loans and turns them into “fixed income” securities. Most debt is “fixed income” if it has a fixed interest rate, a defined principal amount and no payment in kind (PIK) or conversion privileges that make the return something variable.

Sell-side pundits spend countless hours as talking heads on MSNBC, Bloomberg, BNN, Fox Business and CNBC talking about “fixed income strategy”. Am I the only one who switches channels?

Bonds (the primary fixed income security) have a key characteristic - if you buy one and hold it to maturity, you can only get the amount you contracted for - the total of the interest payments and the ultimate repayment of principal. And, while you can’t get more than that, you can get less. A lot less.

The concept of “risk free” rates figures heavily in financial theory based on the popular but specious theory that U.S. treasury securities are more or less “risk-free”. Sure the odds of a U.S. default on those securities is low, but it is not zero. More importantly, the U.S. government talks about curbing inflation but in reality promotes inflation because its tax revenues can not and can never be sufficient to repay the trillions of debt issued, so its only option is to make the eventual principal payments worth less in dollars at the time of repayment than at the time of issue, in effect a “hidden tax”.

Fixed income strategy for fixed income investors as a class is simple. Buy bonds that promise an interest rate that is satisfactory for your needs after adjustment for taxes on the interest and the ravages of inflation and hold them until maturity. Every other strategy will result in gains only if they come at the expense of a greater fool who suffers a corresponding loss and the transactions will attract transaction related expenses like commissions and in some cases custodial fees if you hold your bonds in a brokerage account. It is certain that this class of investors will get less than they bargained for even if some members of the class can profit at the expense of other members through trading.

An example is worth the time to give it some thought. A ten-year U.S. Treasury today has a coupon somewhere in the 4% range and inflation is about 3%. Here is the full-cyle 10 year outcome.

That return ignores the risk of default. Stated simply, your 10-year Treasury was little more than a gift to the government. To come out ahead, you are betting on near zero inflation or deflation. There are better bets.

Many people use investments in fixed income securities to save money for a future purchase of something they can’t afford today - for example, a home. Reality is that “saving” through purchase of treasuries makes realizing that purchase less likely.

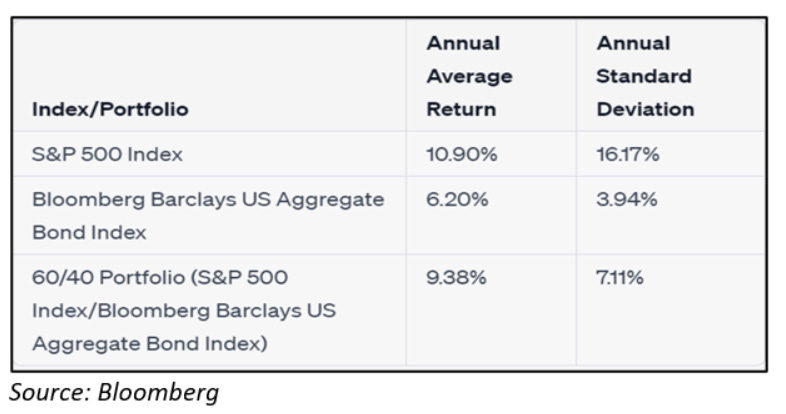

If you really want to save for the long term, either for retirement or to purchase a home, equities (with all their risk) are the only option that is likely to produce a satisfactory result. For the past 50 years, a 100% equity portfolio has produced the best outcomes, albeit with higher volatility.

The returns are not adjusted for inflation. Accepting a lower return for lower volatility is a fool’s game if your investment horizon is long term. For someone saving for retirement 30 years away, the differences are significant.

Value of $1,000 invested in equities, bonds or 60:40 after 30 years, ignoring taxes

Equities - $22,281 or $9,169 adjusted for average inflation of 3%

Bonds - $6,078 or $2,501 adjusted for average inflation of 3%

60/40- $14,607 or $6,011 adjusted for average inflation of 3%

Would you accept 35% to 70% lower retirement income for the benefit of lower volatility? Not me.

Ever wonder why it is so hard to accumulate wealth? Ask your elected representatives, since it is their fault. They claim “price stability” is 2% inflation and appear eager to claim 3% is “close enough” in the face of public outcry of their monetary policies and inane fiscal policies. Price stability is zero inflation, a scenario where governments would have to balance budgets, interest rates would be both “real” and low, and you could save up and actually use your savings to buy your desired home or retire with some certainty about the progress you are making. No candidate for public office would promote such a world since they could no longer use the treasury to buy your votes or claim their fiscal or monetary policy was needed to “promote growth” or “curb inflation”, both claims an outcrop of the dismal set of policies in place for the past 100 years.

If you are serious about accumulating wealth and don’t make your money by managing money for others (a parasitical profession that reduces returns for everyone since advisory fees are not free), buy and hold stocks of well-managed companies that are trading at sensible prices (or temporarily out of favor) and keep them. That has made Peter Lynch, Warren Buffett, John Templeton, Charlie Munger and Stanley Druckenmilller very wealthy and can help you realize your own financial goals.

A good article on fixed income