Fears of a banking crisis are driving investors into money market funds

This trend will be painful for banks but will help the Fed fight inflation

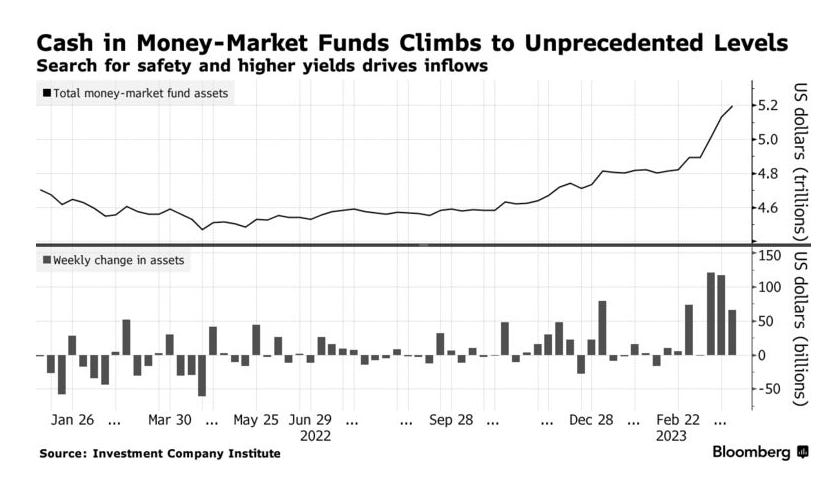

Money market funds dedicated to relatively risk-free Treasuries have seen a flood of cash inflows in recent weeks reaching over US$5 trillion. Much of that inflow has come at the expense of bank deposits. Barclay’s sees the trend continuing. The effect is to shrink the money supply and tighten credit, a goal the Fed is chasing with interest rate rises alone.

While the trend may assist the Fed to fight inflation, it is not constructive for bank investors. As deposits flee banks for money market funds, banks will turn to the Fed to borrow against their “hold to maturity” portfolio of treasuries or simply sell these holdings into the money market funds. The money market funds have the same US$250,000 FDIC deposit insurance as deposits in banks and the value of the treasuries the money market funds hold as assets doesn’t get better just because they are held in money market funds. Those funds may experience their own “run” on deposits if they run short of cash to meet redemptions and are forced to realize losses on the treasuries they hold to earn the interest they pay their own depositors.

As my grandmother used to say, it is hard to make a silk purse from a sow’s ear.

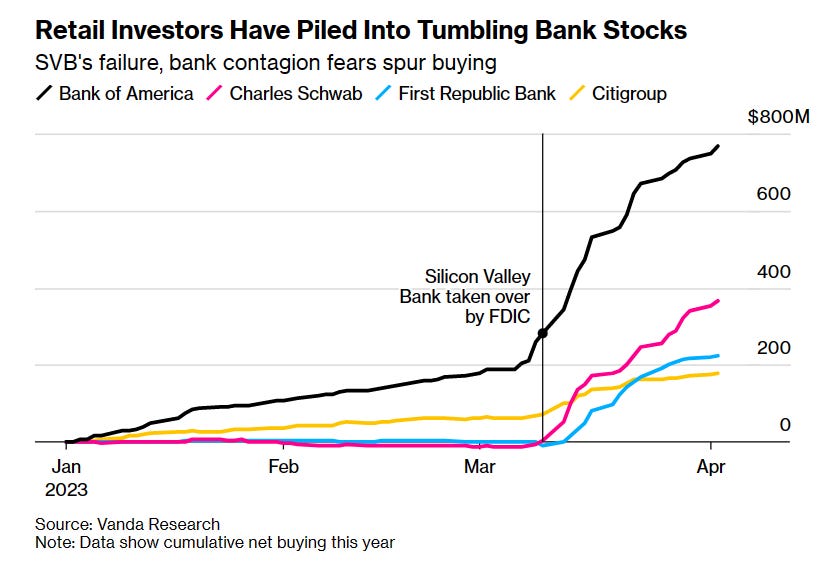

Meanwhile, retail investors are piling into bank stocks at prices they think are “depressed” by the fears of bank failures. Bank failures are an unlikely outcome but lower bank profits are virtually compelled by this shift. With the outflow of money to money market funds resulting in lower deposits the banks will have to shrink their assets or pay higher interest to compete with the money market funds for deposits. If they pay higher interest on deposits, they will need to place those funds in riskier loans to earn a profitable spread. Lower assets and tighter spreads with higher risks in their loan portfolios won’t make bank stocks look “cheap” and as is typical in market turmoil, retail investors will take it on the chin when their “irrational exuberance” has a date with reality.

The rise in mortgage rates has another unpleasant outcome for the banks and for their mortgagees. To avoid foreclosures, banks are extending the term of mortgages for some borrowers and in some cases capitalizing all or a portion of the interest they are owed, adding the upaid interest to the mortgage principal outstanding. The banks will still record the capitalized interest as “income” but it is an issue as to whether they will increase their accounting reserves for future non-performing loans in an amount that recognizes the lower quality of the mortgage portfolio. In Canada, the total outstanding mortgage debt at year end 2021 was $1.6 trillion according to Canada Housing and Mortgage Corporation (CMHC) data. Every one percentage point rise in rates implies $16 billion in higher mortgage servicing costs (not all at once, since mortgages are typically renewed every 5 years and only about 57% of mortgages outstanding are floating rate). Mortgage rates have risen about three full percentage points since the Bank of Canada began raising rates to curb inflation, saddling mortgage holders with $48 billion a year higher interest payments once the full effect of the rise in rates flows through the system and about $30 billion in higher interest payments in 2023 alone. Total banking system profits in Canada by comparison amounted to CAD$46.6 billion in 2019, the latest data I could find.

In my opinion, double digit mortgage rates are more likely than not over the next few years. The Trudeau government keeps borrowing and spending; there is no effort to add to output of fossil fuels needed to fill a growing supply gap; and, wages are lagging inflation - all of which point to higher inflation and higher rates in response. Canada has a robust banking system with good controls overseen by the Office of the Superintendent of Financial Institutions (OSFI) and I dont’ see a bank failure in Canada as a serious risk. Short sellers disagree with me. The largest short position in existence on any global bank today is the US$3.7 billion short on TD Bank.

A collision is coming. Retail investors see banks as bargains and sophisticated short sellers see bank shares as worth “shorting”. Someone is wrong.

What is clear, however, is that 8 years of Liberal government in Canada have created an environment where economic malaise is ingrained and there is no easy way out. Until Canadians toss Justin Trudeau and his NDP enablers out of office and elect a government that will deal directly with the real issues Canada faces, the outlook for the Canadian economy is grim. Do your bit - support Pierre Poilievre and pray he succeeds in his drive to become the next Prime Minister. Your economic future may depend on it.

Common sense tells me banks will be negatively affected by both shrinking margins and lower revenues in upcoming years. I run rough estimations (normalized margin of 15% with 15% discount rate to give space to upcoming recession risk) on several U.S. banks that showed they still have ~30% to go down to be considered “undervalued” except few (C, ALLY).

I spoke with a seasoned Bay St Bank analyst who has seen US hedge funds short Canadian banks 12 times . Their record is 0 for 12 .