Fear has seen investors undervalue Bonterra Energy

A risky but potentially profitable bet on firm commodity prices?

Bonterra Energy (BNE.TO) has been in the penalty box for a few years combining too much debt with onerous debt terms (an effective interest rate of 16%) and the absence of any dividend (which it would be foolish to pay before reducing debt at those rates). The result is classic - investors over react to bad news and fail to appreciate favourable developments and the stock price reflects fear that things will get worse (and well they could).

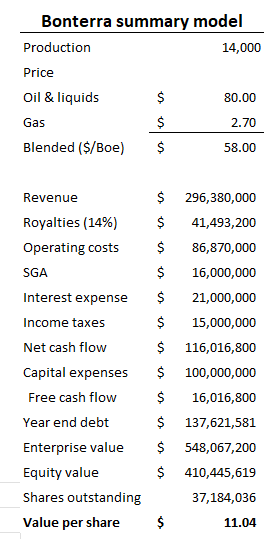

Over the past few years, Bonterra has been putting its house in order. The company should produce an estimated 14,000 Barrels of Oil Equivalent (Boe) a day in 2024 composed of about 6,850 barrels of oil, about 35,000 Mcf/day of natural gas and the balance NGL. At a price of $80 per barrel of oil and liquids (light oil at CDN$95 and NGL at CDN$45 per Boe) and dry gas at $2.70 a gigajoule, Bonterra should produce after tax cash flow of CDN$116 million which, after a CDN$100 million capital program, leaves CDN$16 million to repay debt. Based on a multiple of EBITDA of 4 x Bonterra shares have a value of about CDN$11 based on those assumptions. The stock trades at about CDN$5.00 a share today.

I expect investors will continue to shy away from the stock until meaningfully less debt appears on the balance sheet, so don’t get too excited about the undervalue just yet. But it is useful to run some sensitivity testing on the value of BNE stock at various commodity prices.

The biggest risk (in my opinion) both up and down is the realized commodity prices.

Holding all other assumptions constant and using the above model, I see the following range of share price outcomes based on the following prices for gas:

Price assumption - Estimated share value

$1.00 a gigajoule - $8.30 per share

$1.50 a gigajoule - $9.00

$2.00 a gigajoule - $9.75

$3.00 a gigajoule - $11.25

$3.50 a gigajoule - $12.00

$5.00 a gigajoule - $14.00

I think it more likely than not that the range of $1 to $5 a gigajoule captures the average dry gas price in 2024.

It is useful to do a similar analysis for the price of light sweet crude oil. Given that Bonterra liquids include both oil and NGL, the prices shown below are the oil price assumption but the price used in the model to estimate value include the blended price of both oil and NGL.

Oil price assumption - Estimated share value

$60 a barrel - $1.00 per share

$70 a barrel - $3.60

$80 a barrel - $6.50

$90 a barrel - $9.35

$100 a barrel - $12.25

Clearly, the stock is not without risk. Having said that, there is considerable potential for price appreciation in a firm commodity price environment. Light oil today in Western Canada is about CDN$88 a barrel and at that price Bonterra cash flow is about equal to capital expenditures and potential dividends remain a future hope despite the relatively low valuation.

I hold 50,000 Bonterra shares. I am gambling (there is no better word for it) that Bontera will generate about CDN$15 million in free cash flow in 2024 reducing debt by that amount and setting the table for a larger reduction in 2025 when debt should fall below annual cash flow and free cash flow should support both debt reduction and a dividend. With only 37 million shares outstanding, a fifty cent annual dividend (10% of the current share price) is less than $20 million per year and likely sustainable once debt falls below $100 million. While that may be two or three years away, it is (in my opinion) worth the wait.

Thanks for the write up. I keep meaning to look them up but just don't get around to it. Cheers

Do you have an opinion on Hme and BTE?