ESG investing will cost you money

The pretense that higher costs can be offset by a lower cost of capital is nonsense

The latest fad in managed money is the ESG craze. ESG stands for Environment, Social and Governance and is the outgrowth of the insane idea that corporations (which are legal fictions) should be managed for the benefit of an unidentified group of “stakeholders” comprising everyone but shareholders. The theory is that investors will pay a premium for shares of companies that put social responsibility higher than returns on investments.

What if they did? Shares that sell at premium prices necessarily produce lower returns than the same shares if they did not command a premium price. A lower “cost of capital” is the equivalent of a “lower return on capital”. For a long period, many investors thought a company that could borrow at a lower after tax cost than their return on capital employed would produce higher returns for their shareholders. Merton Miller and Franco Modigliani laid waste to that idea in their Nobel prize winning work “The Cost of Capital, Corporation Finance, and Theory of Investment.”

Their work was correctly criticized for ignoring transaction costs, income taxes and distress costs but they admit that within a relatively narrow range financial leverage can produce somewhat better returns on equity as long as the leverage does not result in the failure of the corporation with equity holders suffering major losses. The number of commodity based companies ( for example Pengrowth Energy, Lightstream oil & gas; Bellatrix Energy; Mercator Minerals; Bonavista Energy) who had outstanding assets but left shareholders with massive losses when they failed illustrates the danger of believing a lower “cost of capital” compels a better outcome, since despite their quality assets they could not meet the payments of their debts when they fell due and went under.

A classmate of mine from my Western MBA studies, Jim Hunter, helped build one of Canada’s most successful mutual fund companies “MacKenzie Financial” before his untimely death from ALS. His success was in large part applying both common sense and prudent valuation methods to investment choices made on behalf of clients. Mackenzie was founded in 1967 and Jim joined as Chief Financial Officer at 1992 after 16 years at Deloitte & Touche. In 1997 he became CEO and led the company until his retirement in 2004. He died at 63 in 2016. His legacy is the impressive growth of the company.

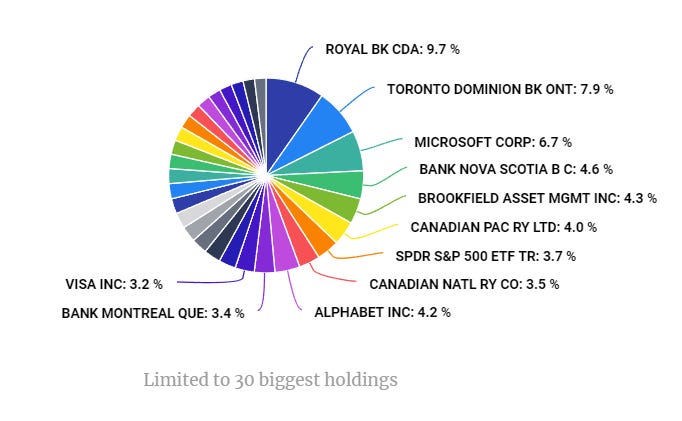

Today, Mackenzie has over $70 billion under management and continues to make its major investments in blue chip North American equities like Royal Bank, TD Bank and Microsoft. This is the sensible approach.

Today, Mackenzie promotes ESG funds as part of its offering, claiming that these funds outperform comparable funds that do not select investments based on ESG. Mackenzie stops short of claiming ESG funds outperform the broad market averages for a simple reason - they don’t.

World renowned valuation expert Aswath Damodaran has explored the theory that ESG investing pays off in an article: “Sounding good or doing good: A skeptical look at ESG”. Damodaran makes no effort to disguise his contempt for the ESG Cloak of Goodness.

I approach this debate on simpler grounds. If ESG has no cost, every company will act to advance the interests of the society in which it operates with care for the environment. That is nothing special, and good corporate governance is common among top companies. But the ESG “aura” comes from measuring something intangible, a subjective view on whether a company has an ESG culture and warrants a prize.

Investors returns in any investment comprise their pro rata share of the return on capital earned by the company, either paid out in dividends or ultimately realized in the stock price. If you add cost, you get lower returns. If a so-called ESG investment improves efficiency, every company will do it as a matter of course and it distinguishes no one.

A favorite argument of those promoting ESG is to claim investors will pay a premium for the shares resulting in a lower cost of capital. As mentioned early in this article, a higher price for shares results in a lower return to the investor, all other things being equal. Stocks are the only commodity on Earth where the buyers seem to want higher prices. That partly explains why so few investors earn returns equivalent to the market indices and most do substantially worse.

Nobel laureate Eugene Fama and Kenneth French demonstrated that two classes of stock tend to outperform the market - those with high book value to market price ratios (relative value) and those with relatively small market capitizations (relative size). Based on this observation, they created the three factor asset pricing model, an advance over the Capital Asset Pricing Model which preceded it in common usage.

Nobel prize winner Richard Thaler demonstrated that buying the worst performing stocks in the S&P Index in any given year and holding those stocks for at least three years outperforms the S&P Index by several hundred basis points, was a founder of Fuller & Thaler Asset Management, Inc. to put this theory into practice.

Quebec’s Caisse de Depot et Placement made the ESG based decision to stop investing in fossil fuel producers and divest such holdings by the end of 2022. The managers made that decision apparently without any concern for their fiduciary duty to the beneficiaries of the Caisse’s investment. Had they made that decision at the end of 2020, the impact on returns would have been interesting.

Year to date 2021, energy was the best performing sector of the TSX index, up some 62%.

The best performing industry was coal mining turning in a return of 256.7%. On the other hand, “feel good” sectors like health care and utilities led the worst performers. Fiduciaries who think ESG will benefit their beneficiaries rather than buying the companies most likely to earn the highest returns will eventually have to explain why their “do gooder” mentality cost those dependent on the returns from the funds they manage so dearly.

If you want to earn higher returns, buy shares when the prices are low based on proven valuation techniques and forget about ESG altogether. Ignore the “sell-side” advisors wanting to manage your money for a fee, a virtually certain way to lower your returns.

Canadian natural gas stocks remain deeply undervalued. Don’t join the left wing parade to allocate funds to ESG investments at the expense of returns. This is the time to add to positions in Birchcliff (BIR.TO), ARC (ARX.TO), Advantage (AAV.TO), Peyto (PEY.TO) and Spartan Delta (SDE.TO).