Do Canadian oil & gas stocks have room to run?

A bit of history helps think that one through

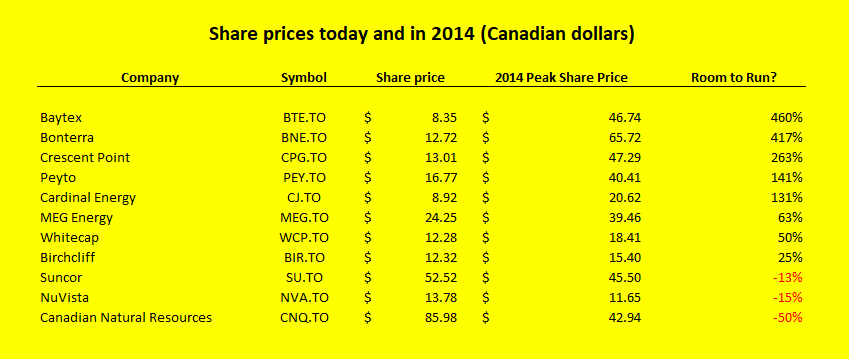

In 2014, the average oil price (West Texas Intermediate) was US$94.41 and the average natural gas price (Henry Hub) was $4.37. Commodity price is the most important driver of exploration and production company profits and in turn share prices. So how do the current share prices of some key Canadian oil & gas companies compare to 2014?

For some companies, mergers, acquisitions and divestitures have made the data not comparable. For others, the company is largely unchanged in terms of its land holdings and economics, and they warrant a closer look.

Baytex has changed with its acquisitions of Raging River and Aurora, but both improved the underlying resources albeit at the expense of excess debt. Those should pay off and Baytex has “room to run”.

Bonterra Energy is largely unchanged since 2014 (it acquired Spartan in 2013) and with a paltry 36 million shares outstanding it should do very well if commodity prices remain firm.

Crescent Point acquired Legacy in 2015, imperiling its balance sheet. That is now under control and the stock has “room to run”

Peyto just keeps getting better. There are no barriers to the company’s “room to run”.

Cardinal’s acquisition of Venturion in 2021 was a risky venture owing to the debt load, but debt is almost gone and Cardinal has “room to run”.

MEG Energy is getting its debt under control and has plenty of “room to run”

Whitecap has been a serial acquirer which saw its debt balloon, but debt is falling fast and the balance sheet is robust. The shares have plenty of “room to run”.

Birchcliff has all but eliminated debt and is no longer highly leveraged. This stock has more “room to run” now than in any time in its history.

Suncor, Canadian Natural Resources and NuVista have done terrific jobs of building profitable businesses with manageable leverage. But in my opinion, they will track commodity prices up and down and are closer to “fully valued” than the other names I listed.

I own Baytex, Bonterra, Peyto, Cardinal MEG, Whitecap and Birchcliff either through shares or options (Baytex, Crescent Point and MEG).

Good luck with your investments. Mine are working out just fine.

As always, Michael, your marriage of historical long view and insightful take on current market state is unique and of immense 'navigarional' value.

I wonder if you might do the same regarding the demand side. Many of us have paltry frames of reference for what "high" really means when it comes to fuel prices, inflation and interest rates (to say nothing of international conflict).

Headlines and analyst outputs are geared to their audiences' recent experience, whereas the 'available present' is always a product of a somewhat deeper past.

Thank you Michael for your priceless insights. You are not only enriching a lot of Canadians but also helping revive Canada's O&G companies and economy.