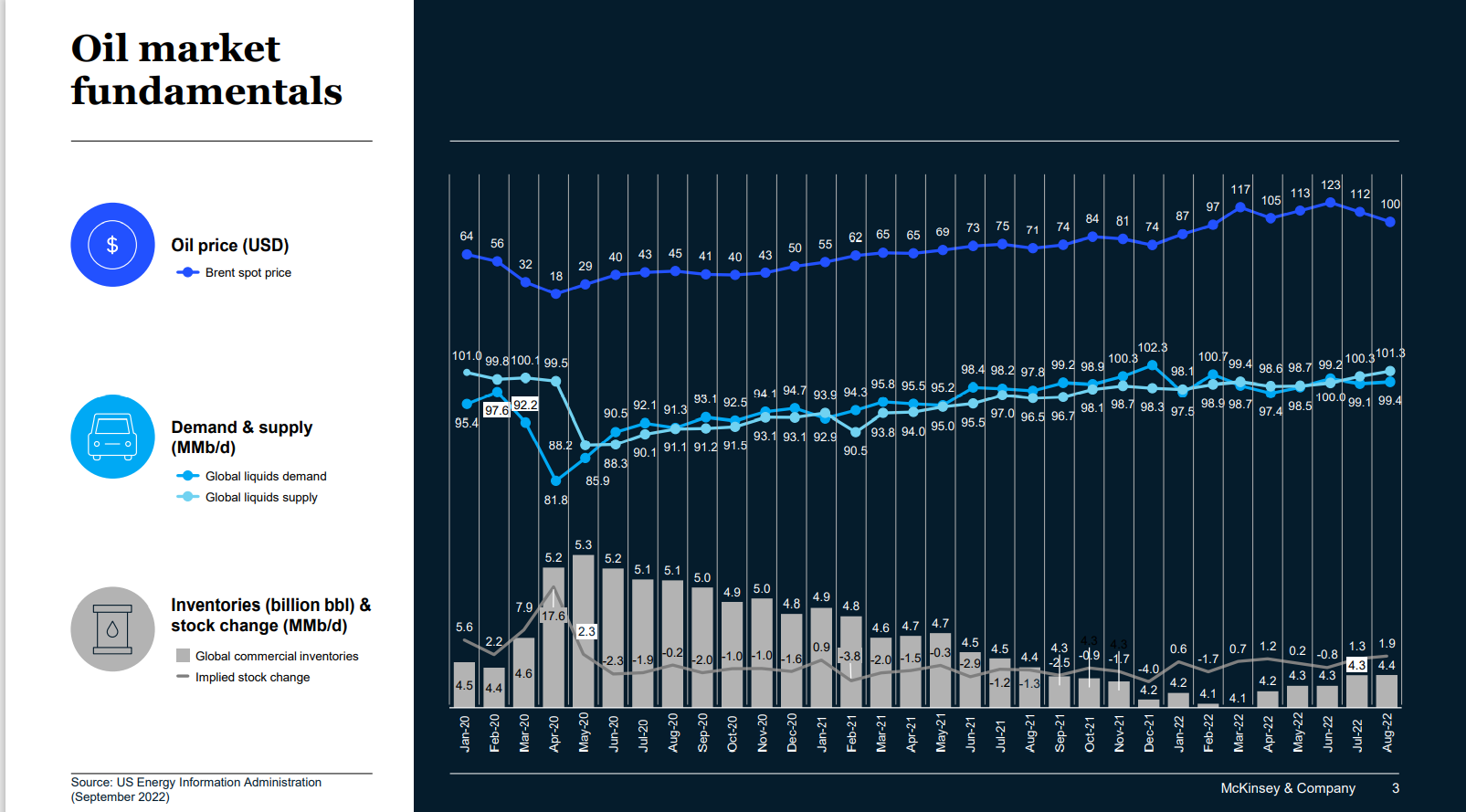

Declining global oil inventories point to higher prices

Governments cannot wish away the global energy shortage

My old employer, McKinsey & Company, Inc. recently published some interesting data on the global oil supply and demand balance since the start of the pandemic in 2020. The data point to declining inventories and stable demand.

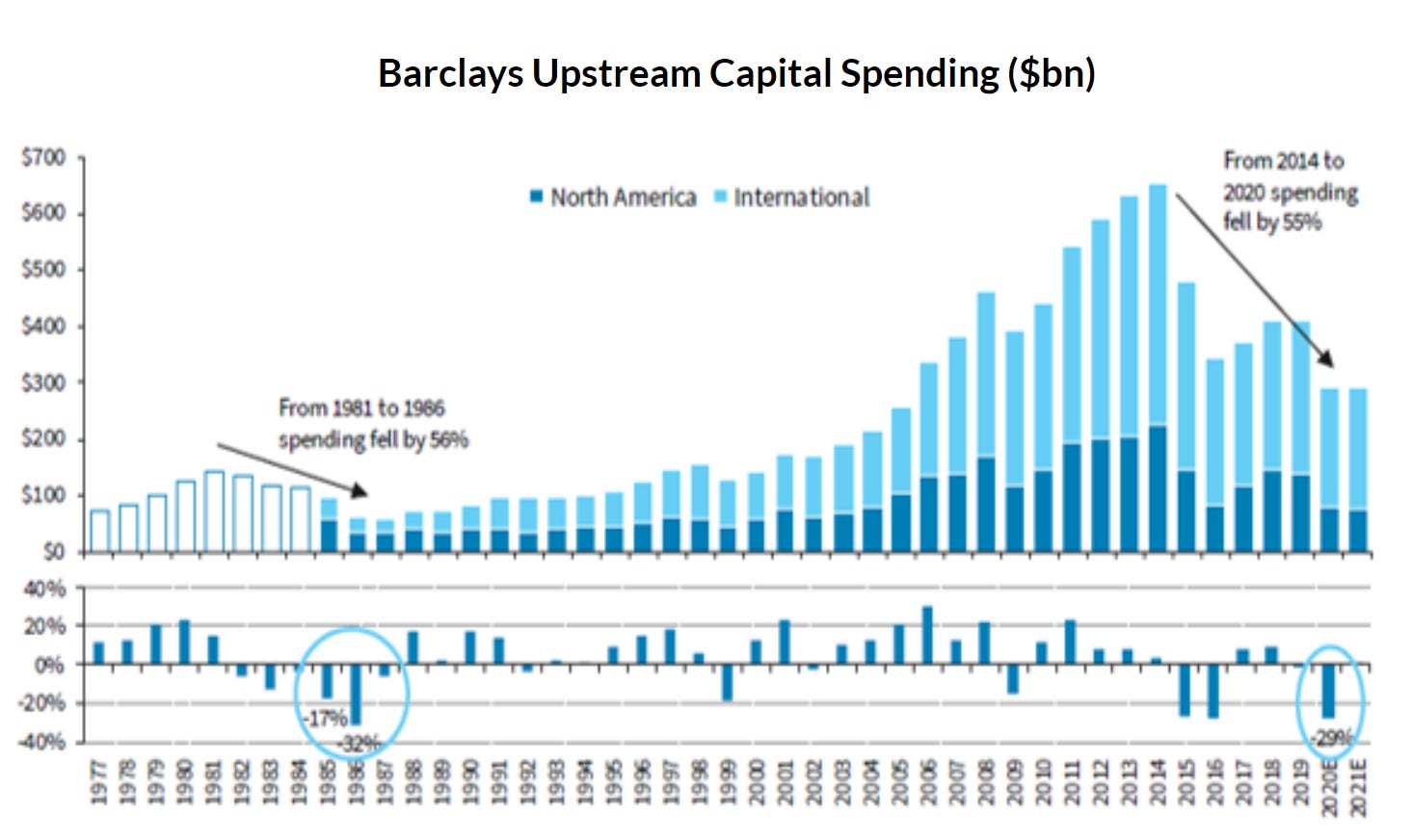

The global shortage is the result of capital fleeing the oil & gas industry in the face of relentless attacks on the industry in the name of “climate change”. Annual capital spending has fallen by hundreds of billions of dollars per year since 2014. With oil wells suffering natural declines in output, the lack of spending manifests itself in declining supply. Inventories are being consumed to make up the difference.

It is not that energy companies are not generating cash flow. They are but they are preferring to repay debt, increase dividends and repurchase shares for cancelation. This chart from Eric Nuttall at NinePoint Partners estimates the percentage of free cash flow being returned to shareholders by quarter throughout 2023 according to company plans.

Eric is famous in the energy space for two reasons -

First, his fund turned in a return on investment that led the mutual fund industry for the past 2 years and was only modestly worse than my own (Eric’s fund returned 163% in 2021, my portfolio returned 189%).

Second, Eric is obsessed with the time it would take a given company to go private by using their free cash flow to repurchase shares which is his preferred use of free cash flow.

I think Eric understands energy but it is clear to me he has a lesser understanding of corporate finance. The assumption that repurchases over a three year period can be made at today’s stock price is specious and a bit silly. It is a bit like a belief that takeover targets will being willing to sell to a seriously low bid. The reality is that a company that undertakes a major issuer bid will be arbitraged towards fair value by investors, including those whose M&A spreadsheets have been looking at the particular company as a target.

It is not just the silliness of thinking investors will sell below fair value over an extended period but also the dream that the stocks are “cheap” at today’s price when Eric was AWOL three years ago when the same companies were trading at a fraction of today’s price. Where were the buybacks in 2014, or in March 2020 when stocks like Birchcliff (BIR.TO) and Whitecap (WCP.TO) for example traded below CAD$1.00 per share and no one was eager to use cash flow to repurchase shares? Why is it a better use of funds to repurchase shares of those companies at prices close to CAD$10.00 a share only two years later?

Buybacks benefit fund managers and brokers and, if it works for them, those benefits must come from investors since no one else is present. With free cash flows of around 30%, Eric sees “buybacks” as a good use of capital in the same presentation where he touts the payback on drilling in the Marten Hills Clearwater area of about 3 months. When the return from drilling is 400% in one year, buybacks are a waste of opportunity and a poor use of capital. The buybacks might drive the share price higher in the short term, increasing the management fees for Eric’s fund by increasing the “assets under management” but the higher prices mean lower returns for the marginal investor and leave the investors who didn’t sell into the “buyback” exposed to the next pandemic, recession, etc. which can happen a lot earlier than the 3 year horizon.

I argue that higher energy prices are likely and that the best use of capital is first to fund expanded supply which the world desperately needs and which offers the highest return on capital with payouts on drilling of one year or less, and then to pay dividends which benefit all investors without dividing them into groups - one which sells out into a buyback and one which remains at risk. In his own fund, Eric frequently trades into and out of positions as his views on value change, but buybacks deny investors the same opportunity since they are stuck in the stock unless they sell and compelled to increase their risk in the buyback company or expose themselves to trading costs to rebalance their holdings. Small investors would be driven into odd lots by such an event with even higher trading costs.

The risk to energy investors is a change of administration in United States and Canada to one that favors energy independence to the inane “climate change” nonsense driving policy today. In Canada, Pierre Poilievre would support dramatic expansion of Canadian production and pipeline construction and I suspect Ron De Santis in America would do the same if he runs and is elected President in 2024. Rapid expansion of oil & gas is essential to avoid a global economic collapse and leaders will eventually figure that out, putting an end to the global shortage long before any of the E&P’s listed by Eric would be able to “go private”. Markets correct for everything over time and an analyst or fund manager who thinks he or she has unique insight is likely to be spanked as their obsession with a short term market anomaly collides with reality.

For this winter, I think gas producers couldn’t add production quickly enough to stave off the winter shortage I foresee and investors will benefit from holdings like $BIR, $PEY, $TOU, $NVA, $CNQ, and $PNE to name a few that I hold.

Thank you so much for taking the and write your analysis and thoughts.

As an investors in the space, I am fascinated by your thoughts.

Between Eric, Dr Anna's and yourself, I am able to get a be/er clarity of the space, specifically canadian oil stocks, where I am fully invested in the last 2 years.

Keep up the great work, and thoughts coming.

Disagree completely on buybacks. Most tax efficient way to return money to shareholders. Finance 101, M-M Theorem. As for the number of years to take a company private, no one believes the share price won't move, the point is illustrate how low valuations have become and buybacks force a revaluation or else you sell cheap. If people want to sell cheap I'm all for it.