Citi has been a chronic loser for years

But there seems to be some value that might surface

Trading at about half book value, Citibank (C) hasn’t done investors any favors for quite some time. Citi stock was as high as ~$80 in May of 2021 and today languished just over $50 a share. It is a chronic case of poor management of a terrific franchise.

Banks are relatively easy to value if they are reasonably well managed. There is cash or equivalent on both sides of the balance sheet and a bank that can earn the cost of capital of the Standard & Poor 500 should trade at or near book value. Citi has a book value of $92 a share but trades well below book. Why?

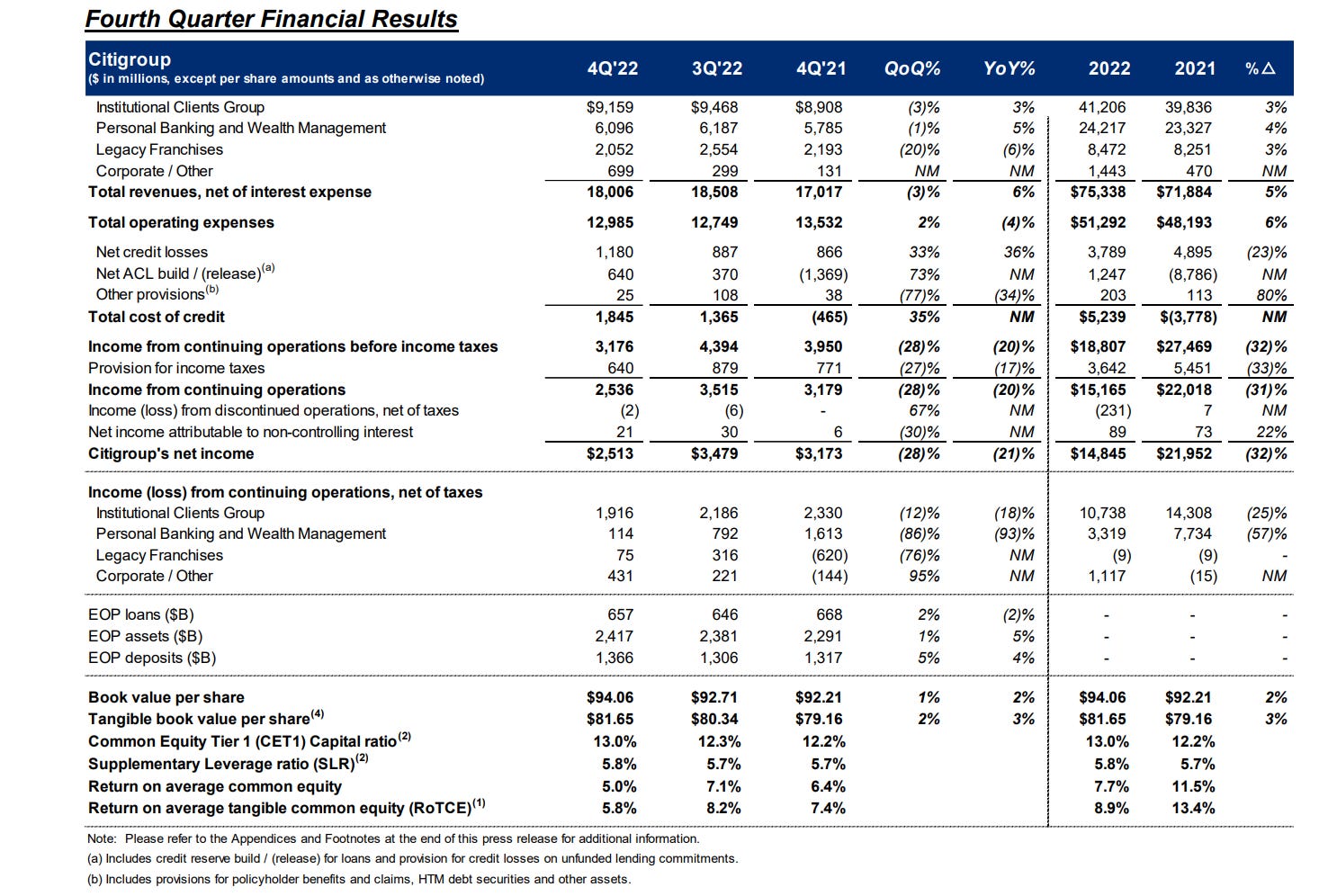

The answer is a pretty jaded track record of volatile results and an opaque mix of business segments making it difficult for even a Nostradamus to accurately project earnings or exposure to losses. 2022 didn’t make that any easier, with income from continuing operations falling 25% in the Institutional Clients Group and 57% in Personal Banking and Wealth Management. These segments could be renamed - Institutional Clients Group might better be called “Exposure to weak credits” and the “Wealth Management” part of personal banking might better be named “Wealth Destruction” based on 2022 performance.

But there is nothing wrong with Citi’s accounting that I can see, and better management might see the company valued at or above book value, like all of the Big Five Canadian banks which trade between 1.3 and 1.8 times book value. Why do I see value? Firstly, Wall Street analysts are becoming a bit more bullish.

Secondly, the long expected U.S. recession keeps getting swept ahead of reality as unemployment falls to the lowest on record and businesses keep buying back stocks (almost $1 trillion of buybacks in the year ended March 2022 and plenty since). Companies flush enough buy back stock are signaling that they are overcapitalized and by corollary are strong credits. Loan losses among institutional clients don’t seem likely to become a runaway problem. At the same time, the torrid pace of buybacks is keeping a floor under the wealth management business and the inverted yield curve should permit Citi to widen the spread it earns on loans and fixed income.

Poor management can screw up anything, but the environment to me seems positive for Citi and investors with strong stomachs can nibble away at the stock at a deep discount to intrinsic value, hedging a bit with covered calls. The ~4% dividend together with call premiums of about 10% for a 1-year call open the door to a return in the 15% range by buying stock at $51 and writing the January 2023 $52.50 call at $4.75 premium. The return to call if held to maturity is on the order of 20%, higher at annual rate if called out early. Given the size and scale of Citi, it is possible to put on a reasonably sized position with the risk of loss limited to share prices below $45.00 or so. Citi stock hasn’t been that low for about 20 years.

Like all stocks, an investment in Citi has risk as well as potential reward and a deep recession can take the bloom off the rose. But I like the odds on this one.

By my estimate (and I’m not good at it yet, just learning) Citigroup is 50% undervalued based on normalized margin (15%), 12 years of future growth of 5% and 15% discount rate. It looks cheap related to other banks, probably for a good reason. But if they overcome their issues - good gains are ahead. I’m establishing small position and will add time to time.