Chesapeake is becoming a juggernaut

The Southwest merger makes the company a "must own" in the natural gas space

A blockbuster merger between Chesapeake Energy and Southwest Energy creates one of the largest North American natural gas producers with the added benefit of some US$400 in synergies. The merged company’s output will start at about 7% of total U.S. natural gas production or in the range of 7 Bcf/day. For Canadian investors, that is about three times the size of Tourmaline (TOU.TO) and five times the size of ARC Resources (ARX.TO). Enterprise value of about US$24 billion is the likely trading range when the merger closes.

Initial debt of the merged entity will be about US$3 billion, and the company expects to pay that down quite quickly reaching a leverage ratio of 1 x EBITDA within a year. Based on current prices, dividends (fixed and variable) should total somewhere around US$1.4 billion, over 6% annually.

Chesapeake is a low cost natural gas producer with economics somewhat similar to Tourmaline Oil and the fit between CHK and SWN is exceptional given they operate in the same basins with excellent access to major markets including LNG exports.

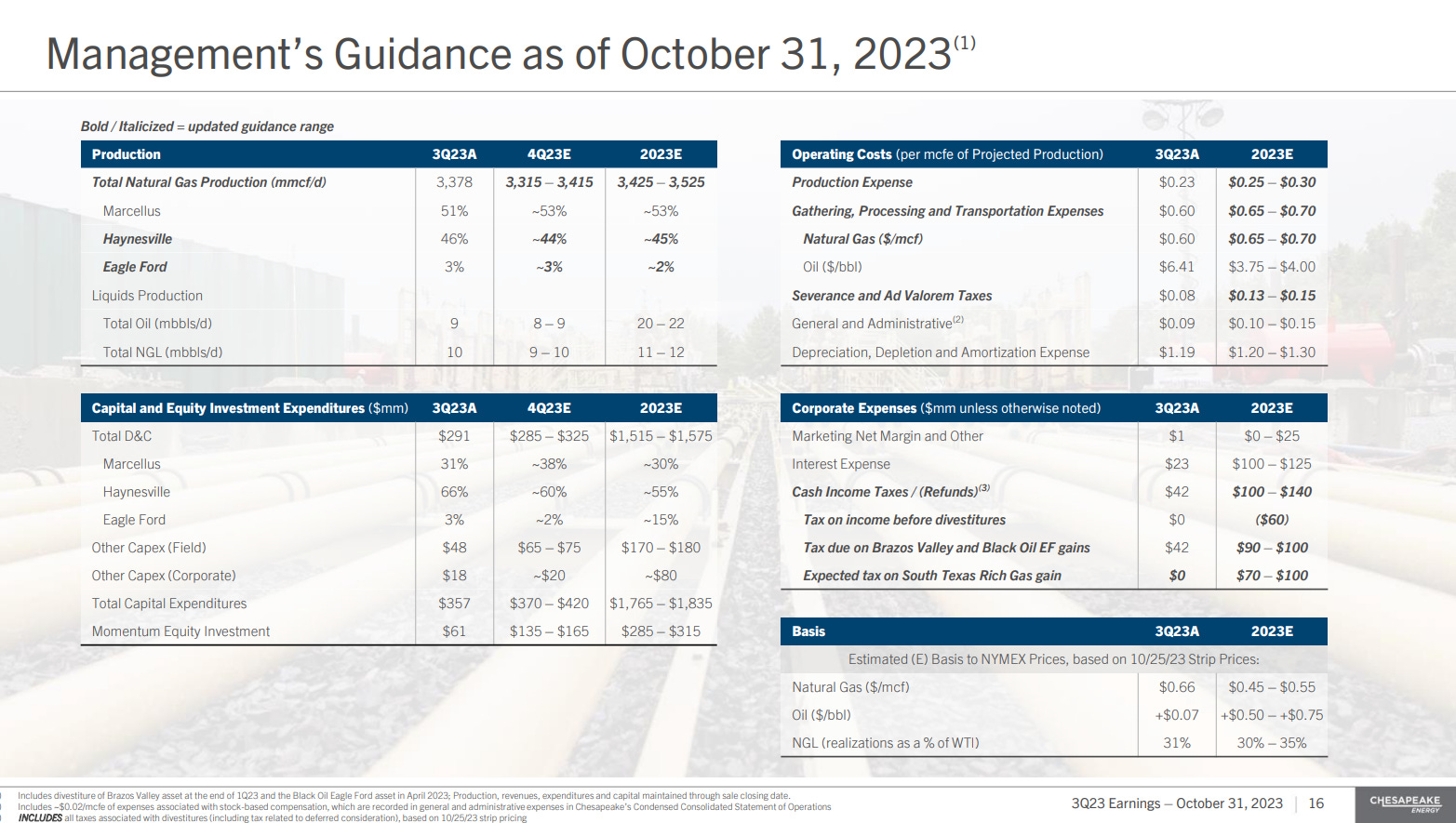

With costs per mcf in the US$0.60 range, CHK should be cash flow positive at natural gas prices as low as US$1.00 per mcf and hedges its forward exposure to lower prices with a systematic hedging program similar to $PEY.TO which many Canadian investors will find familiar.

Chesapeake stock currently trades in the US$80 per share range and I value the shares post-merger in the US$120 range at natural gas realizations in the US$3 per gigajoule area. Netbacks from LNG exports are likely higher than domestic prices and the diversified access to markets offers some protection against local price weakness.

More data will be released in the next few quarters but the merger looks strong enough that I have added some CHK options (January 2026 expiry at US$60 strike price at a cost of US$24 per option) so the potential gain if the market prices trades to the value I see is more than a double in two years.

There is always a risk the merger will not proceed, and despite recent strength in natural gas prices, a sharp price decline cannot be ruled out. This is a high risk, high reward bet. While my position is options, if the world unfolds as I project I will exercise my options and hold the shares long term. If not, my exposure to loss is limited to the option price and the premium over intrinsic value was only US$4 per CHK share, so the likely outcome is better than holding the stock directly and the risks seems lower to me.