Chesapeake Energy offers low risk and high leverage to natural gas prices

The company has come a long way since Aubrey McLendan

Founded by Aubrey McLendon and an early star in the U.S. natural gas market, Chesapeake ran into rough waters when natural gas prices plummeted in the wake of rapid growth in production as “fracking” took off. McLendon, a genius by many reports, drove his SUV into a bridge and killed himself one day after being indicted for “bid rigging”. Over aggressive expansion fueled by debt ran directly into the fall in natural gas prices and the company entered bankrupcy, emerging in 2021 as a “new” Chesapeake, listed on Nasdaq as CHK.

The stock has been on a tear ever since, and has a rock solid balance sheet today bolstered by the recent sale of assets not considered “core” by management. Eagle Ford oil assets were sold to INEOS Energy for $1.4 billion and south Texas assets to Wildfire, also for $1.4 billion. Those asset sales reduce the company’s debt to an insignificant level.

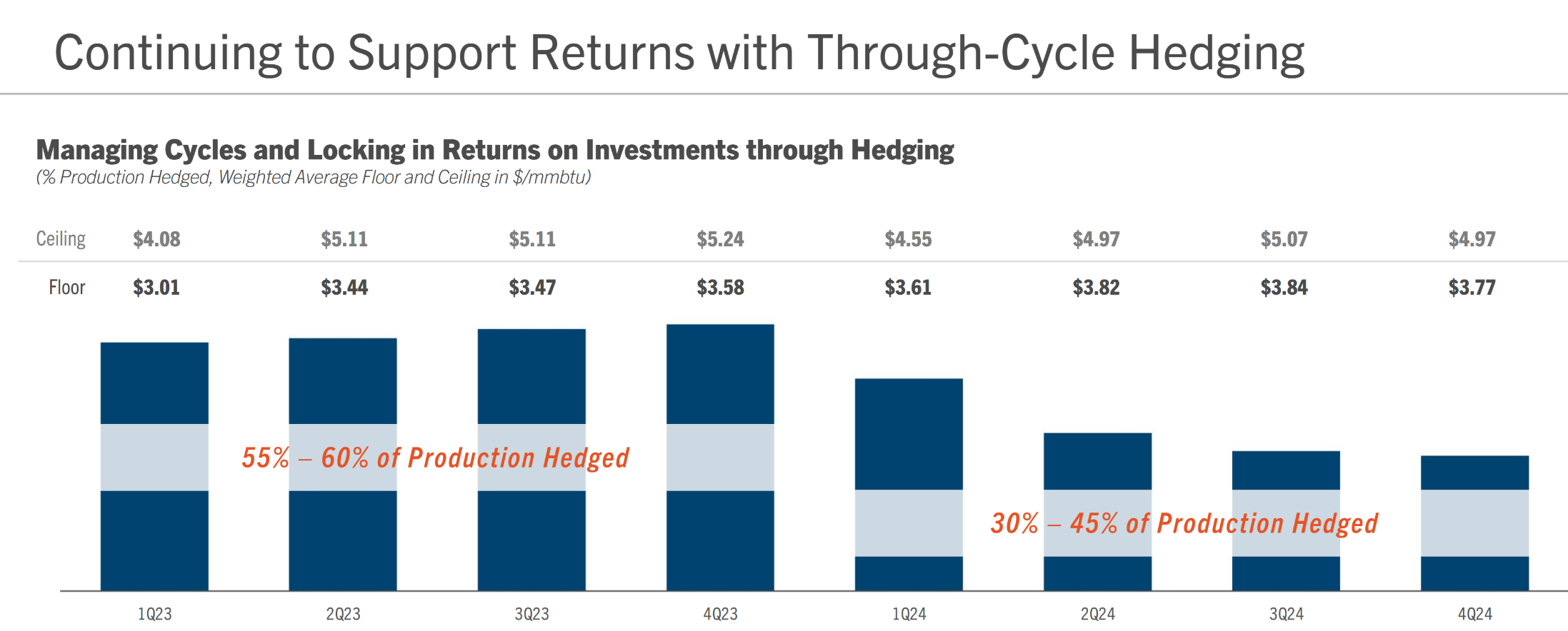

Chesapeake stock’s rise has been stalled by the fall in natural gas prices from a Henry Hub price of about $10 per gigajoule just a few months ago to the $2 range today. With costs of about $2 a gigajoule, investors seem concerned about short term profits. I am not. The company just reported full year 2022 results with net income of $24 a share and tons of free cash flow. For 2023, Chesapeake has about 55-60% of its natural gas production “hedged” at $3 to $3.50 per Mcf which assures positive cash flow for this year, and has pulled back on drilling cutting a few rigs.

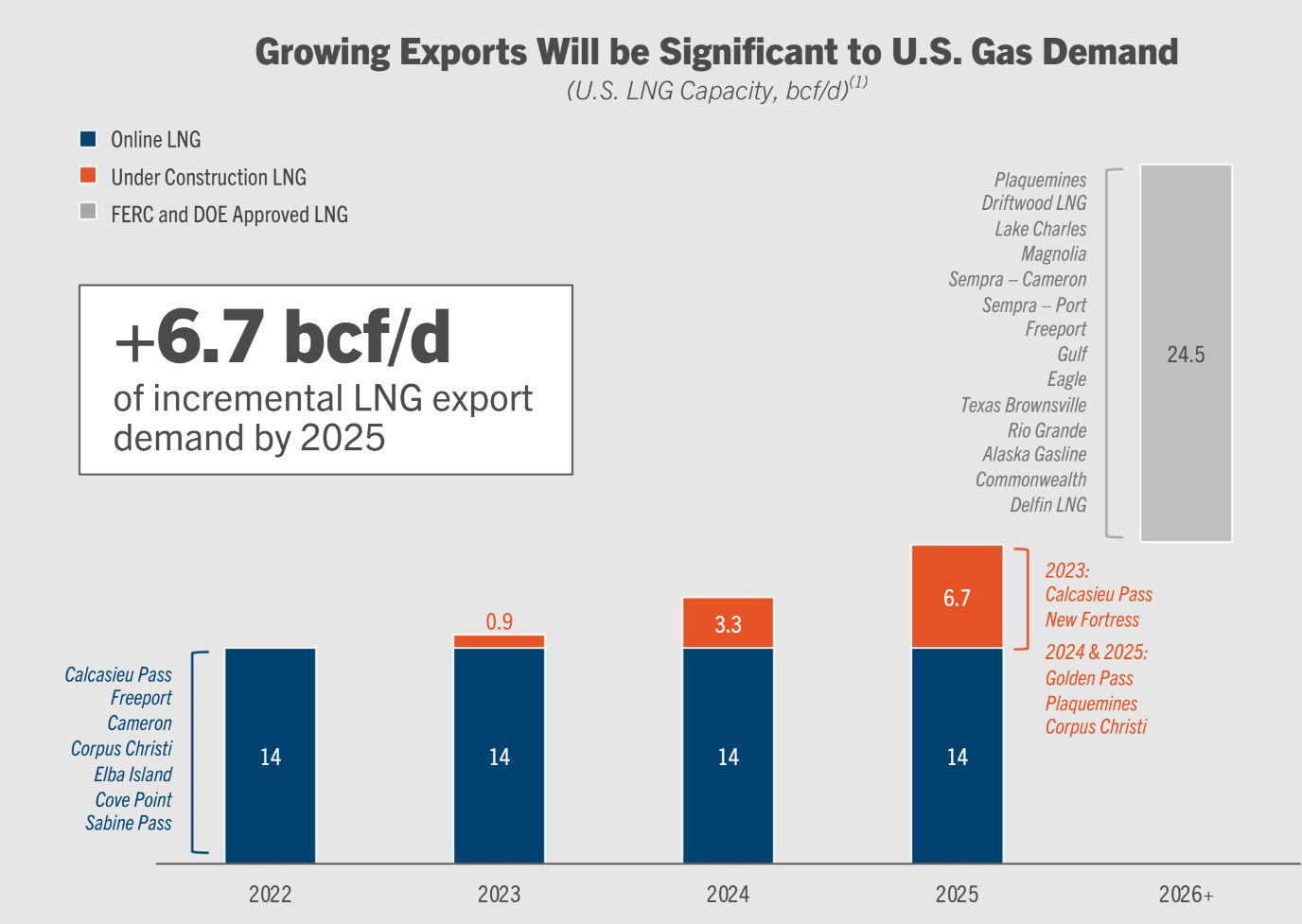

The warm winter and Freeport LNG facility fire created a short term oversupply of natural gas but those factors are not permanent. Freeport is now starting up and will eventually return to its 2 Bcf/day capacity shipping gas to gas starved Europe, and (unless you have bought into the “global warming” scam promoted by left wing leaders lide Biden) there is no reason to believe winters will be as warm as this one in perpetuity. The soft natural gas price is (in my opinion) an opportunity for energy investors, Chesapeake pays dividends from its free cash flows, and I am bullish on natural gas long term. The company’s dividend rate will rise and fall with its ability to generate free cash flow and is currently set at $2.20 a share “base dividend” with extra dividends when cash flows permit. The company says its dividend is covered down to $2.40 per Mcf natural gas prices, a bit higher than today’s price so don’t expect any special dividends until prices are higher.

I have opened a position in Chesapeake and will add to it over the summer months if the weak gas market persists. At about $80 a share, CHK trades at a low multiple of earnings and cash flows, has a fortress balance sheet, and operates some of the best natural gas assets in United States. Growing exports of LNG are a tailwind for North American natural gas producers.

In my opinion, Chesapeake is undervalued.