Chapter Sixteen: Efficient Investing in Inefficient Markets

Overleveraged companies can be as much opportunity as risk

Companies that become burdened with excess debt often look like terrible investments and most of them are. But sometimes the beaten up equity provides a substantial opportunity when the company recovers from the doldrums of the debt penalty box. Knowing which is which takes some work.

One valuation approach that works well is one that recognizes that the equity of a leveraged company is much like a call option on the assets of the company with a strike price equal to the debt and duration equal to the average duration of the debt. Sound a bit confusing. This article by famed valuation expert Aswath Damodaran who teaches Advanced Valuation to graduate students at the Stern School of Business at New York University is worth taking a moment to read. The “value” of the equity is analagous to the value of an out-of-the money stock option on a volatile security. If the assets of the company rise in value to where they exceed the face value of the debt, the equity becomes valuable. The assets may rise and fall in value without any change to their cash flows simply because the market is affected by the level of interest rates (lower rates often drive higher asset values), changes to the tax regime, advances in technology, value of the operating assets to a competitor, new intellectual property, and so on.

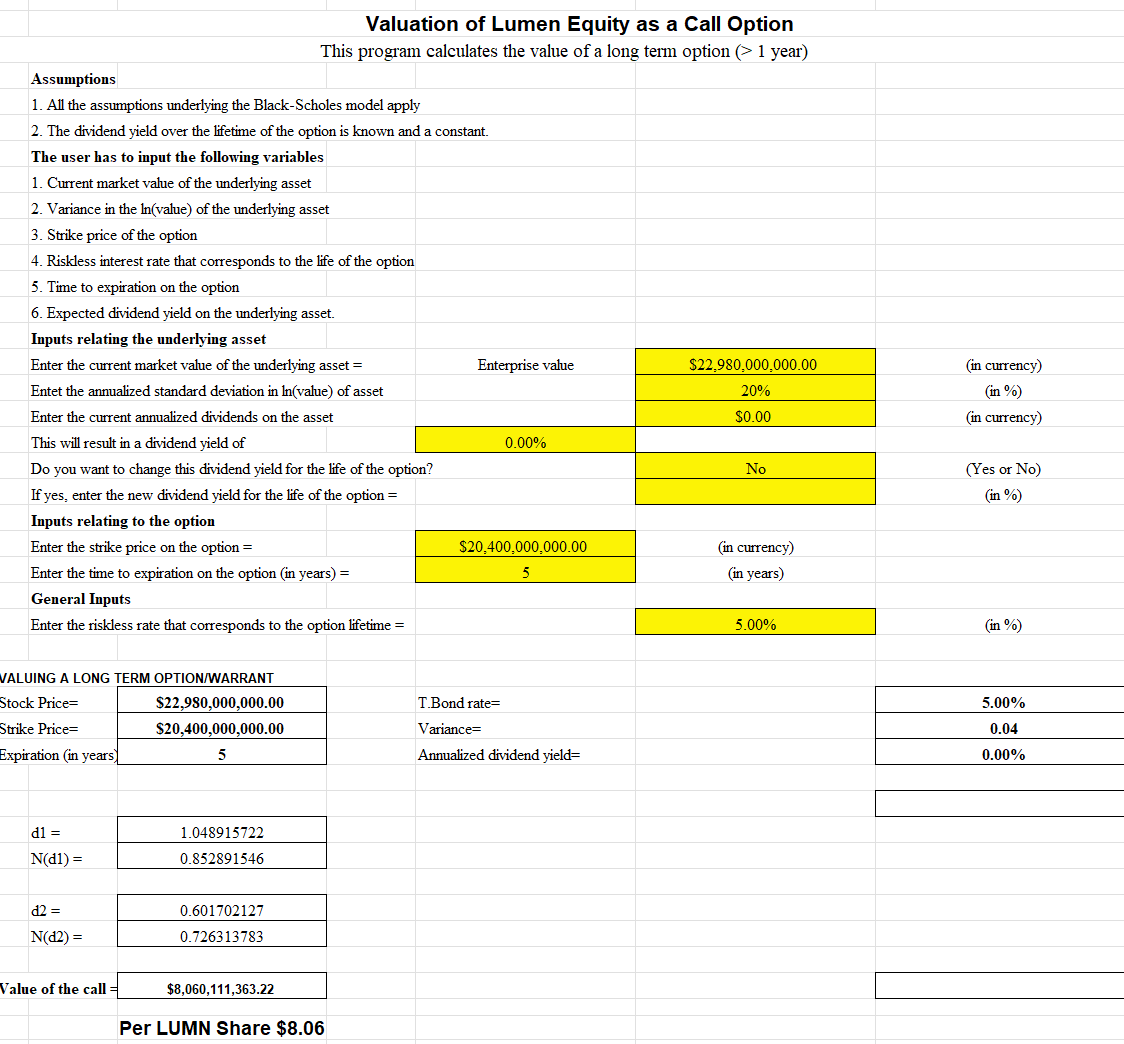

Lumen Corporation (LUMN) is a good example. This software company bills itself as “Enterprise Technology for the Digital Revolution” and is profitable, more or less, despite carrying some US$20 billion of debt on top of a market capitalization of only US$2.58 billion (one billion shares outstanding trading at US$2.58). If Lumen can’t meet its debt obligations it will fail and its assets will be auctioned off by the receiver. Shareholders may receive nothing.

But if Lumen can manage its debt, keep generating positive cash flows, and increase sales and profits, equity holders can do very well. As Professor Damodaran argues, the equity can be fairly valued as an option. Eyeballing the term structure of Lumen debt (don’t hold me to precision) I see it has a duration of about 5 or 6 years. I will use five years for my valuation since that is plenty of time to see whether Lumen can gain control over its finances or otherwise.

Using a 5-year risk free rate of interest of 5% and a volatility of 20% the calculated value of LUMN share is over US$8.00 versus a market price of US$2.58. Brave investors can buy the stock with a decent chance of a triple and an approximately equal chance of a total loss of their investment.

Ordered Aswath‘s book about valuations. Hope to get more literate at it.