Chapter Seventeen: Efficient Investing in Inefficient Markets - Hidden Gems - Gibson Energy

A classic case of dividend growth

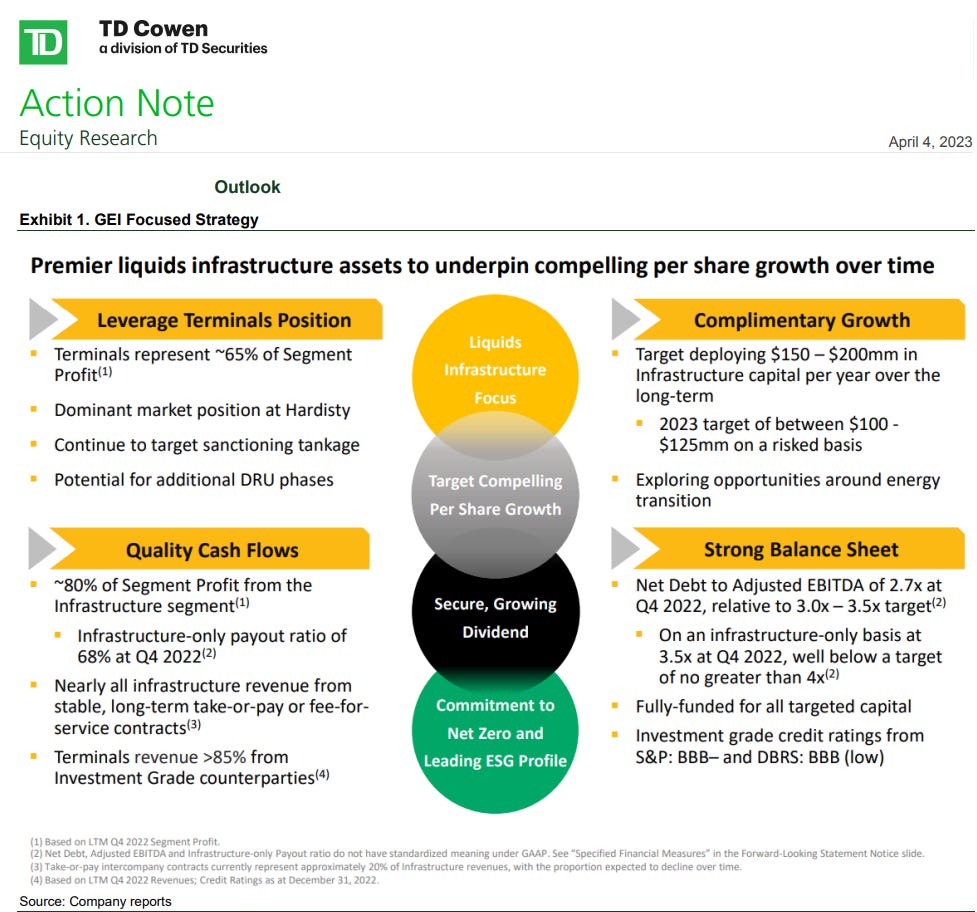

TD Cowan sees Gibson Energy (GEI) as “undervalued” owing to recent weaknesses in share price “performance”. Like most sell-side analysts, analyst Linda Ezergailis, P. Eng. thinks higher share prices benefits investors when in fact lower prices do, but recognizes that growing dividends (a corollary of lower stock prices) provide long term value.

Gibson Energy (GEI) currently has a dividend of $1.56 and yields 7.2%. Gibson’s dividend has grown by over 5% a year for a few years and the runway ahead suggests that rate of growth understates the company’s ability to pay dividends. This is a classic case for the Gordon Dividend Growth Model (GDGM). The value of Gibson shares using the GDGM and a 9% “required rate of return” [approximately equal to the return on public company shares making up the S&P index for the past 50 years) is $1.56/ (.09 - .05) = CAD$38.75.

Wise investors will see the opportunity to add Gibson shares and hope the market continues to undervalue the shares so they can add to that holding by reinvesting dividends to build a long term source of growing income. Traders are too eager to see prices rise, sell for a gain, and face the burden of not only paying commissions and a tax on the gain but also of finding another investment with long term prospects as good as the one sold.

I see Gibson as a great addition to an energy portfolio in this risky market. Buy it, hold it and sleep well at nights.