In March of 2020, the announcement of COVID19 spooked investors who, true to the findings of behavioural economist Richard Thaler, ran for cover and abandoned investments in well managed and profitable companies, particularly in the energy sector. Oil prices fell sharply and the investing public concluded it was a permanent change - a nonsensical view that the world could operate without the benefit of the energy contribution of fossil fuels. That opened the door for investors to buy public company shares at a tiny fraction of their intrinsic value.

Buying well-managed companies’ shares when they are out of favor is a successful strategy. In the case of the COVID19 scare, the opportunity was profound. Very little money was needed to buy relatively large positions, albeit with risk.

Some notable “bargains” included:

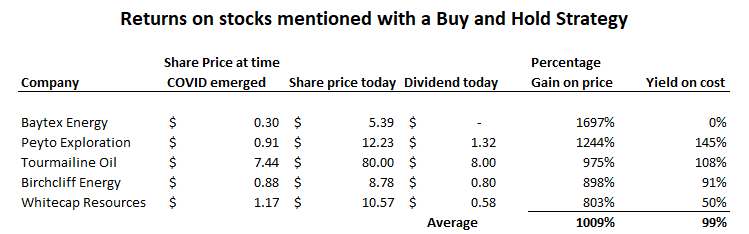

Birchcliff Energy (BIR.TO), a low cost natural gas producer, whose shares fell to CAD$0.65 on March 27, 2020.

Whitecap Resources (WCP.TO), a well-run oil producer whose shares fell to CAD$1.17 on March 1, 2020.

Baytex Energy (BTE.TO), a Canadian E&P with excellent assets but too much debt, whose shares fell to CAD$0.30 on March 22, 2020.

Tourmaline Oil (TOU.TO), Canada’s largest natural gas producer, whose shares fell to CAD$7.44 on March 15, 2020.

Peyto Exploration (PEY.TO), Canada’s lowest cost natural gas producer, whose shares fell to CAD$0.91 on March 1, 2020.

There is no doubt that these companies would have been in danger of a liquidity crisis if the low commodity prices persisted for several quarters. But investors should remember the old energy industry adage “the best cure for low prices is low prices”. Oil & production suffers natural declines if insufficient capital is spent to sustain output, and when prices fall dramatically, capital spending is curbed as well. The following table illustrates the benefit of this “buy out of favour stocks” strategy over the 3 years since COVID appeared in China - average returns over 1,000% and a dividend yield based on cost averaging 99%.

Why did I choose these stocks and how would you be able to make similar choices? As I mentioned, two factors are in play - a serious sell off in stock markets and a choice of investments based on formal valuations.

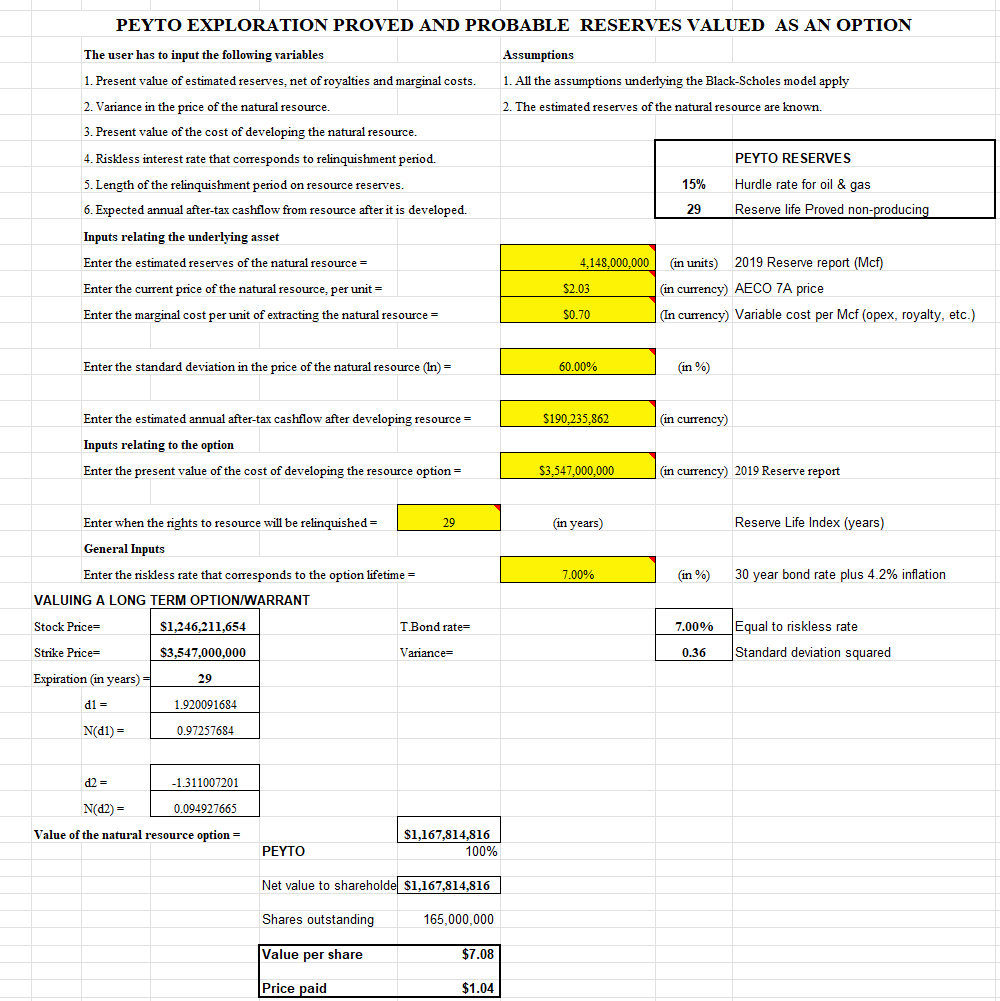

Let me run through the math on why I invested in Peyto Exploration. Peyto is Canada’s lowest cost producer of natural gas, and has positive cash flows when its rivals are bleeding cash at low commodity prices. Peyto has extensive reserves and owns its own infrastructure. I did a modified Black Scholes valuation of Peyto’s reserves to decide whether it was worth buying when the market tanked. I dealt only with Peyto’s natural gas reserves, ignoring both the value of its 123 million barrels of oil and natural gas liquids and its extensive infrastructure which alone would cost over $1 billion or $6 a share to replace.

I came up with an intrinsic value for Peyto’s gas reserves alone of about CAD$7.00 per share based on natural gas prices of $2.01 per Mcf (AECO 7A) and variable costs of $0.70/Mcf including $0.12 royalty and $0.19 transportation to market. Here is that valuation

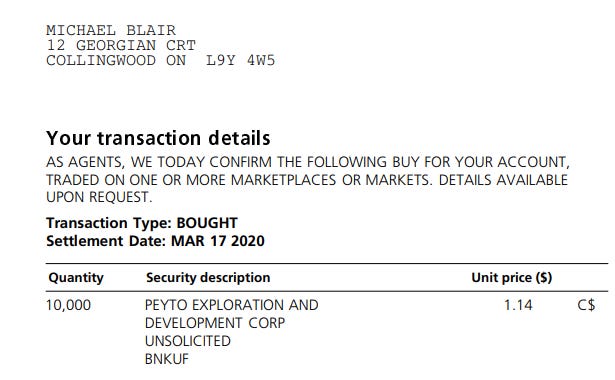

With infrastructure alone having a replacement cost a multiple of the stock price and my rough valuation of just Peyto’s gas reserves also a multiple of the stock price, I concluded the shares were deeply undervalued. Based on my confidence Peyto was undervalued I began to buy shares. Here is a trade ticket for one of those trades. I still own Peyto shares. Sure, there was plenty of risk given the company’s billion dollar debt, but on balance there was significant opportunity.

Investing is work if you are serious. It is a dangerous hobby if you are not. The key to finding “hidden gems” is due diligence and effort. If you plan to invest material amounts of money in a given company’s stock, it is not a financial advisor you need, it is a competent business valuator if you lack valuation skills.

Once you have acquired a holding in a profitable, well managed business, stop checking the stock price every few hours and deal with it like you house or car. You own it, and the day to day trades by others are of no consequence. Of course, follow the company’s public disclosures to assure yourself there has been no fundamental change in its business but otherwise leave it alone and let it work for you. If you owned a shoe store, a barber shop or a restaurant you would not try to find out its market price every few hours or days or panic if it had a bad month. Think of your investments in the same way.

In the next chapter, I will give another example.

The article is a keeper! tks

Thank you Michael and congratulation for your work