Chapter 21: The most successful investment fund in history

You hardly ever hear of Jim Simons today

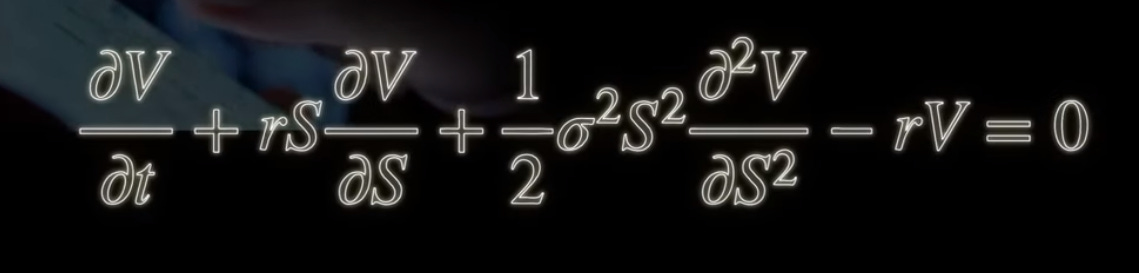

In 1988, a mathematician named Jim Simons started the Medallion Investment Fund and ran that fund for the next 30 years with a compound rate of return of 66% over the period. A $1,000 investment in his fund at inception and held to maturity was worth billions of dollars when Simons retired from management. He didn’t use charts, earnings multiples, tarot cards, tea leaves, crystal balls, or advisors - he used mathematics. His investments were guided in part by the 1973 paper by James Merton called “The Pricing of Options and Corporate Liabilities”, which when adopted and published by Myron Scholes and Fischer Black became known widely as the “Black-Scholes, Merton” model of option valuation. Their work followed theories advanced by Louis Bachelier (Brownian movement, an important concept in physics), and Edward Thorp (a Blackjack researcher applying probability and statistics theories to Blackjack and to markets generally).

But Black-Scholes applies to a lot more than stock options. The concept is simple - for any risky asset there is a price that represents an equivalence between the risk of loss and the potential for gain which incorporates the return on a riskless asset and the variability of outcomes on the risky asset (often called “volatility”). The arithmetic is complete with only the inputs of “riskless rate” and “volatility” requiring analysis, judgment or guesswork. It resulted in what I believe is the most important financial equation in the history of finance. In the equation, S is the current price of the asset (or the cost to develop the asset in the case of physical assets such as resource company reserves), r its the riskless rate of return, and V is the output of the equation, the value of the “option” which might be an option on a stock or the optionality presented by ownership of an asset such as resource reserves.

Even companies that are over leveraged can be subject to valuation using Black Scholes, with the amount of debt its duration set as the “strike price” and “duration” of the option and the current enterprise value analogous to S - the current price of the asset. The equity which may comprise no tangible net worth is valued as a call option on the company’s assets which can vary in value all the way until an insolvency event or even beyond that event if the company is not liquidated in bankruptcy.

Venture capital investments can be reasonably valued using the Black Scholes model.

The days of discounted cash flow ((DCF) and net present value (NPV) are not gone, they are supplanted by insights developed using Black Scholes, and Black Scholes is a more robust approach for companies where the primary drive of profit and loss is (for example) the global market for a commodity or a natural resource reserve, the prices of which cannot be reliabily forecast or determined by the efforts of management. DCF and NPV have value only where a reasonable forecast of future cash flows is possible and has some level of substance. Black Scholes does not need a forecast since its only subjective inputs are measures of volatility and riskless returns, which, while subjective, have more validity than forecasts of future commodity prices.

To control for possible errors in estimates of volatility, a Monte Carlo simulation is a simple step running the Black Scholes model across a wide range of volatility metrics that judgment leads the analyst to conclude captures the expected future volatility with some accuracy. No investment is “riskless” but an implicit riskless rate of return is equal to long term treasury bond rates adjusted for the rate of inflation, since any other rate will suffer from the change in the value of money over the life of bond. At a macroeconomic level, real GDP is a proxy for a riskless rate of return since investors who do not earn returns equal to or greater than real GDP growth are losing money relative to markets generally over time. Many academics suggest the inflation adjustment is to subtract expected inflation from the treasury bond rate, which I see as perverse logic since to offset inflation and still have a positive return a higher rate is needed and the treasury rates suffer from government intervention and do not capture the price discovery of a truly free market. A four percent bond rate with 5 percent inflation rate leads to a perverse conclusion that a riskless investment declines in value over time. I argue that the implicit riskless rate equals the short term bond rate plus expected inflation, rather than the 10-year rate less inflation that many economists prefer. In periods free from central bank intervention, these approaches are not widely disparate.