Changing household versus government debt has tilted traditional economic analysis on its ear

Tweaking policy rates just doesn't work any more

This is a follow-on article to a previous one arguing that higher rates no longer curb inflation unless those rates are very high, but focuses on Canada.

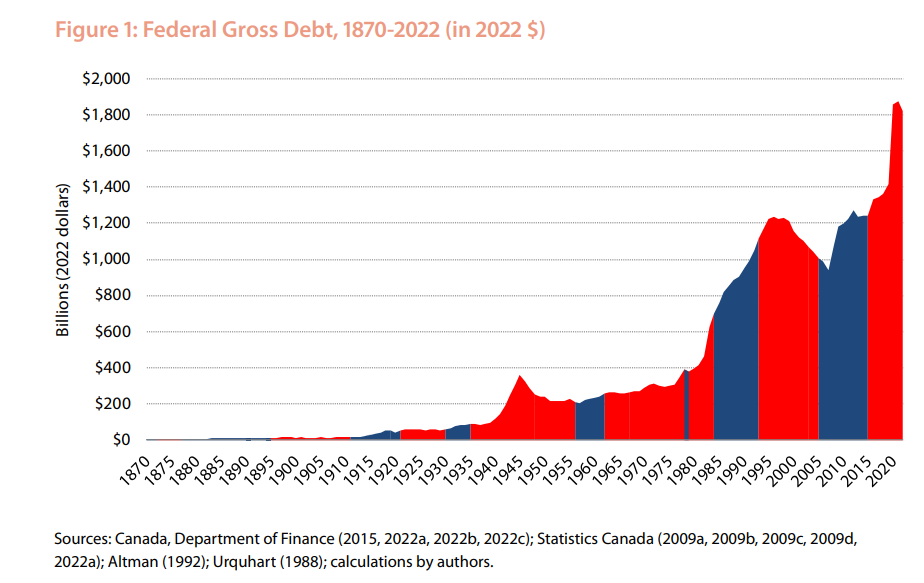

In 1980, Canada’s national debt was less than $400 billion and per capita amounted to about $15,000.

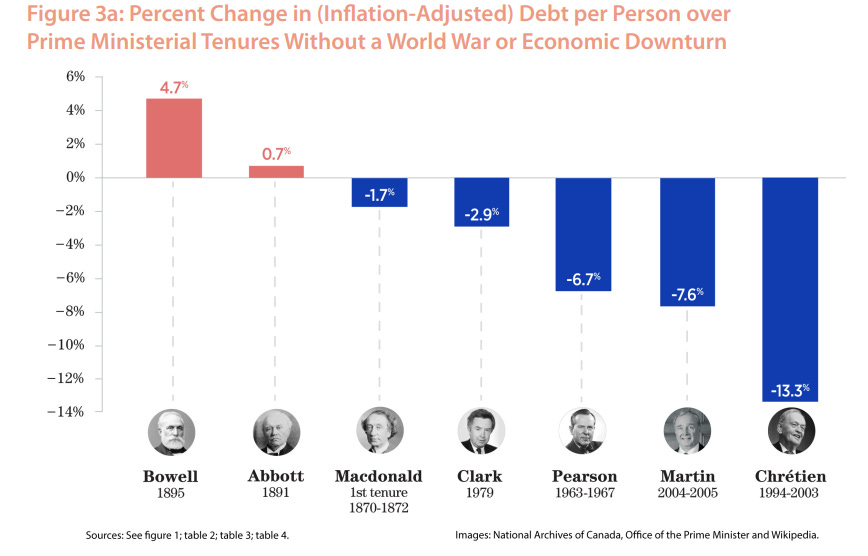

Liberal and Conservative Prime Ministers presided over reductions in national debt per capital through to the end of Jean Chretien’s time in office, excluding the World Wars. Canadian leaders used to understand that national debt is debt owed by the citizens, since the government is a legal fiction incapable of repaying debt without taking money from people.

Over time, both governments and families use of debt increased, great for bankers but a problem for economists trying to assess the impact of policy choices. In 1980, Canada’s economy (GDP) totaled $275 billion or just over $11,000 per capita. Household debt comprised less than half of GDP or about $130 billion. Canada’s population was a bit less than 25 million. In those days, a 500 basis point rise in interest rates amounted to about $6.5 billion additional interest costs on household debt added about $1,000 to the cost of living for a family of four. There was a mild offset in the higher rates which produced more interest income for debt holders, but much of that debt was held abroad and the interest income was subject to tax while interest expense was not deductible in Canada.

With consumer spending making up about 60% of GDP in 1980, that $6.5 billion higher interest cost reduced consumer spending by 4%, enough to reduce GDP growth by 3%. Monetary policy was at least theoretically effective in controlling inflation by cutting consumer demand and in turn reducing employment. Even in 1980, a 400% basis point rise in rates was insufficient to curb inflation and rates kept rising into the teens and low twenties before they did enough economic damage to affect rising prices.

Fast forward to 2024. National debt is now $2.2 trillion. Population has grown to 40 million. Consumer debt is also $2.2 trillion, $1.8 trillion of which is mortgage debt. A 500 basis point rise in rates has somewhat different effects than in 1980.

The rise in interest rates increases payments to government debt holders by $110 billion (once all lags in refinancing are taken into account). About 70% of Canada’s debt is held by Canadians, so the increased interest payments provide $77 billion more income to those investors. Almost half of Canadian mortgage debt is fixed rate, and in the short term unaffected by the rise in policy rates. Mortgage rates have risen by less than the Bank of Canada rate increases but have nonetheless risen by about 400 basis points in this rate cycle. The drag on the economy from higher mortgage rates is about $850 million x 4% = $34 billion.

Higher rates on consumer loans flow right through to reduce consumption. The drag on the economy from 400 basis points higher Bank of Canada rate is $500 billion x 4% = $20 billion.

The Bank of Canada hopes the higher rates will curb inflationary pressures but the large fiscal imbalance isn’t helping, a point made publicly by Bank of Canada governor Tiff Macklem. In addition to the $40 billion budget deficit, the higher rates are now stimulative rather than restrictive.

Higher rates on government debt owed to Canadians added $77 billion to consumers’ incomes

Higher mortgage rates took away $34 billion

Higher consumers loan rates took away $20 billion

A $40 billion fiscal deficit is money transferred by government to individuals

The net result of these conflicting policies is $117 less $54 gives a stimulative affect of $61 billion, about $10,000 for a family of four.

The thought that Bank of Canada policy rate rises will stifle inflation is a pipe dream. Higher rates will cripple the economy and trigger insolvencies and business failures but rates will need to be much higher to impact inflation or may not be effective at all given the lack of consistency of fiscal policies under Trudeau. Lower rates will ease pressure on households but will fuel higher inflation when coupled with deficit spending.

The Trudeau government has led Canada into a fiscal trap from which there is no “soft landing”. Righting the ship will be painful and with Trudeau in office unlikely. The Liberals will keep borrowing and spending desperately trying to retain power in the face of their terrible poll results which show the party losing ground in spades.

Until government spending is reduced to at least a balanced budget or surpluses, economic growth will tick higher, inflation will persist, and home prices will remain elevated both in terms of rent and mortgage carrying costs. In the face of persistent inflation, Bank of Canada policy rates have nowhere to go but higher.

You can fix policy but there is no fix for stupidity.

https://youtube.com/watch?v=RWoRs5UtvmI&si=S-VyyASCwzD4v9wN

Only 8 minutes long … Don Drummond was a senior mandarin for several PMs in his day , a centrist, common sense economist