Canadian real estate prices may be heading for a crash

Another Trudeau government policy failure

Almost everyone I know who owns a home congratulates themselves on their presience in buying when they did, and crows about the tax free gains they have enjoyed or will enjoy when they sell. My first wife, Nancy, still owns the modest subdivision home we purchased in 1978 for about $120,000 funded in part by a 7% mortgage. A few years later we nearly lost our home when rates surged to 18% and our monthly mortgage payment approached my take home pay. Fortunately, I was made a Vice President of GE Canada not much later and my first bonus allowed me to repay the mortgage.

In 2005, I assited Nancy to build a new house on the property at a cost of about $1 million. Nancy has decided to sell the house now and move into a nearby condominium penthouse. Local realtors tell her she should list the home at $4 million. Based on my review of homes near hers, she is likely to get more.

A few weeks ago I published an article setting out the case that today’s nosebleed housing costs were a policy failure at all levels of government. Driven by a combination of inadquate supplies of serviced lands, artificially low interest rates and governments pandering to developers (often with corrupt officials involved) and immigration policies letting families enter Canada at a rate greater than residential construction can accommodate. Canada’s home prices are overvalued today. It is not just me who says so.

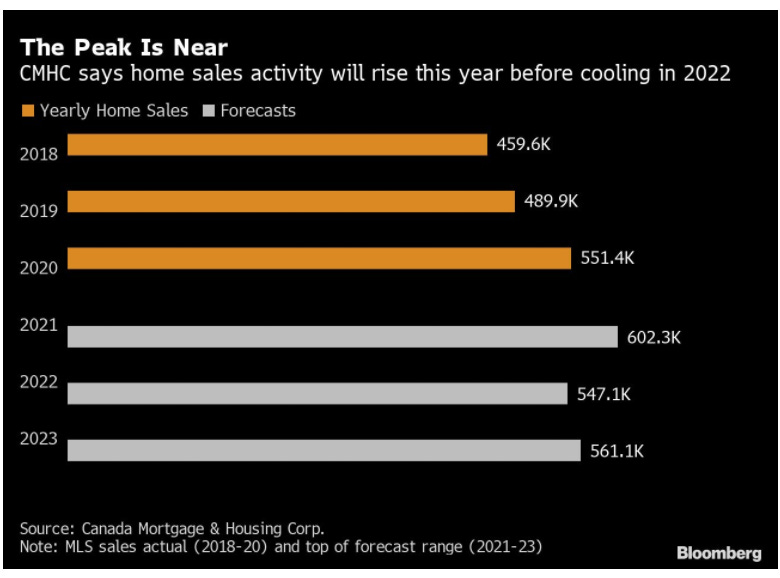

Moody’s says Canadian home prices are overvalued by 91%, but that firm does not expect prices to fall any time soon. Deutsche Bank says Canadian housing prices are the most over valued in the world, but sees the over valuation at 60%, somewhat less than Moody’s. In all markets, over valuation can persist for extended periods which gave rise to the old saw “markets can remain irrational longer than most investors can remain solvent”. Canada mortgage and housing corproation (CMHC) sees home prices rising futher thinks they peaked in 2021 and will ease in 2022.

So why do I think a crash is possible, even likely? Two words - interest rates.

Canadians owed about $2 trillion in mortgage debt. A 1% rise in mortgage rates adds about $20 billion to carrying costs for the approximately 10 million Canadian households or about $2,000 per household. By some estimates, 53% of Canadians are within $200 a month of insolvency.

Canadian inflation (in effect, a tax on the poorest in society) is now running at 4.7% annual rate and in my opinion more likely to rise further than to abate. In parallel, the Trudeau government speech from the throne implied higher taxes were likely as our federal government funds its “climate change” narrative not the least of which will be increases in the so-called “carbon tax”. The government will soft pedal taxes by pretending that increases in corporate taxes are paid by corporations rather than simply passed on to those corporations’ customers which, of course, they will and must be. Corporations don’t pay taxes, they collect them. Anyone who thinks otherwise needs a course or two in economics.

Tiff Macklem, governor of the Bank of Canada, has already admitted that rate rises are likely and has ended Canada’s Quantitative Easing (QE) program which held rates at bay by buying bonds. Macklem,Trudeau and Minister of Finance Crystia Freeland will try to keep up the pretense that rate rises will be gradual and modest as long as they can, but reality will set in as a global energy shortage (the result of poorly considered “climate policies”) continue to drive up energy costs and wage pressures from unions struggling with inflation find their way into our productive sectors. If the relentless pressures of energy costs, supply chain disruptions, wage demands and profligate government deficit spending persist, rate rises of only 1% are a pipe dream.

Canada has chosen to elect ideologues rather than leaders with knowledge and competence. Those elected leaders will continue to promote unchecked immigration, higher carbon taxes, outright war on our energy industry, and a plethora of costly “feel good” programs that squander precious resources. The effects will be felt first in the housing market as those with variable rate mortgages suffer immediately and those with fixed rate mortgages have to roll over that debt at higher rates.

My own experience with out of control inflation in the early 1980’s left me with enough scar tissue to recognize the signs and symptoms of poor government policies and the platitudes our leaders spout when things turn south, hoping that soothing words combined with hopes and prayers will pay the bills. This will be an ugly ride, in my opinion, so buckle up.