Birchcliff Energy: The market is not buying it

But I am and you might

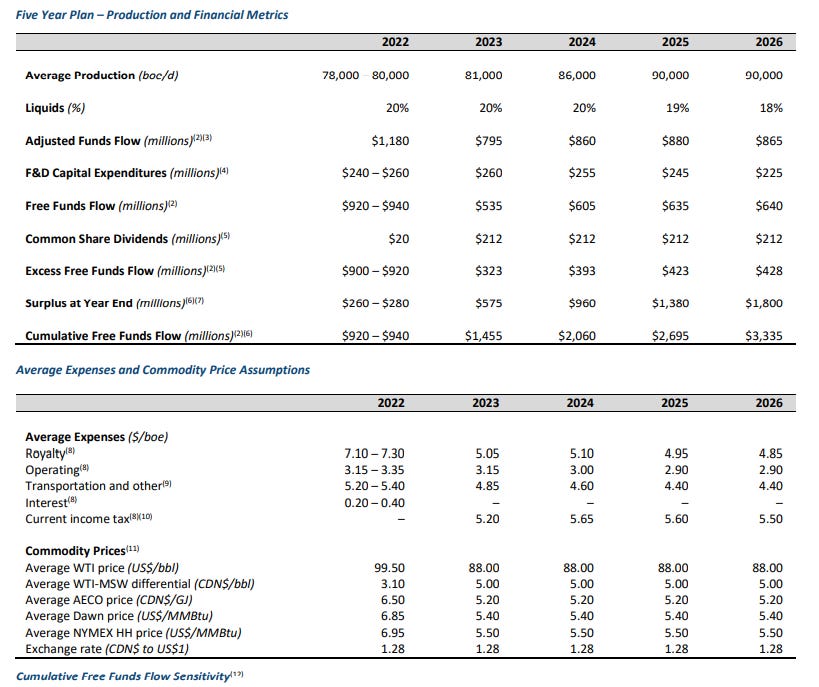

In its Q1 2022 Birchcliff (BIR.TO) released a 5-year plan which showed a massive build up of cash on the balance sheet even after a dramatic increase in the divident beginning in 2023 and the company becoming fully-taxable on its income. Here is that plan:

Over the next 5 years, Birchcliff projects CAD$3.3 billion of free funds flow, or about CAD$12.50 a share. Cumulative dividends during the period total CAD$868 million or CAD$3.25 a share. There is plenty of room for higher dividends despite the projection including income taxes paid of about CAD$650 million.

Mr. Market is valuing BIR.TO shares at CAD$8.00. Either Jeff Tonken is full of crap or Mr. Market has it wrong. I am going with Tonken. His projection is not based on some airy-fairy forecast of high natural gas prices, but on a flat CAD$5.20 per gigajoule. The current Canadian natural gas price is over CAD$7 per gigajoule.

At a 4 x EBITDA multiple, Birchcliff shares would have an end of period value of around CAD$20 a share. The present value of that dividend stream and terminal value is CAD$16.20, about double the current price.

Of course, if natural gas prices collapse the value will be lower and if they surge the value will be higher. World prices for natural gas are a lot higher than those in the Canadian market, with prices as high as US$35 a gigajoule in United Kingdom, Europe and Asia. With Europe now dependent on LNG imports from North America, I expect the North American price to slowly migrate towards the European price and while I don’t see US$35 a gigajoule, it is not hard to envisage a world where North American natural gas prices of CAN$10 or higher prevail. They have been that high before.

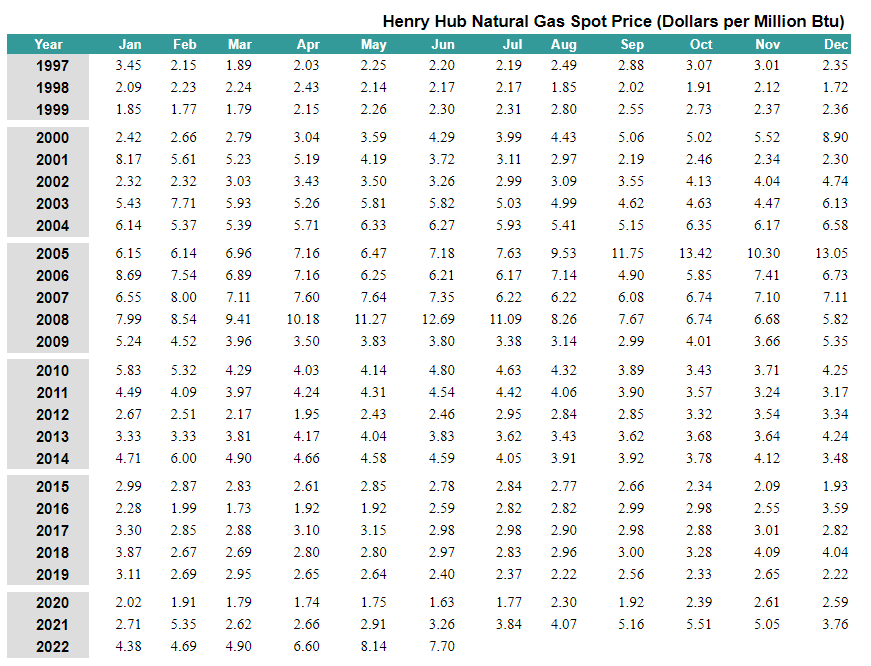

Source: Energy Information Administration

What I see in Birchcliff is a soon-to-be debt free and profitable company planning to pay a dividend which at today’s stock price provides a yield of about 10% with plenty of free cash flow that more than exceeds the planned dividend.

Accoringly, I hold 80,000 shares and expect I will add to that holding.

Tonken has it right! My top long position is BIR.TO ! I am enthusiastic about planned dividend increase in 2023 (80cents/share/year).

Hi Michael, I am a new subscriber to yours substack. Many thanks in advance for all the valuable knowledge you are imparting. Few questions on your thesis on Birchcliff.

1) Why do you think that Birchcliff has one of the best management teams in the industry? Can you give some of the reasons for that? What have they done historically to merit that high praise?

2) Being unhedged looks great when the gas price is high. However, they can go down as well in the near future (like WTI has been in a downtrend for the past few days). From my novice point of view, I have always think of hedging as a downside protection but capping the upside benefit as well. What are some of the best practices for hedging that the companies should employ?

3) It seems like Birchcliff can get debt free at the end of the year if the strip prices remain close to where we are? Based on that, Birchcliff promises to 10x its dividend. WOW!! Have you seen that happen before with other companies, and how do you analyze such claims? (I have been dinged by Shell before, so just want to be cautious with these high dividend yield players, Birchcliff's yield will go to 8-9% when they 10x the dividend in Q1'2023)

4) In the worst case scenario for gas price, can you guide us with an easy 'thumb of rule' or 'back of envelope' calculation, that gives us a rough estimation of what Birchcliff could make in such a scenario?

5) What is the lowest gas price you expect based on worsening fundamentals and supply/demand data?

Many thanks for your guidance in advance.