Baytex is too inexpensive to ignore

Baytex is too inexpensive to ignore

Market inefficiency creates opportunity for the brave

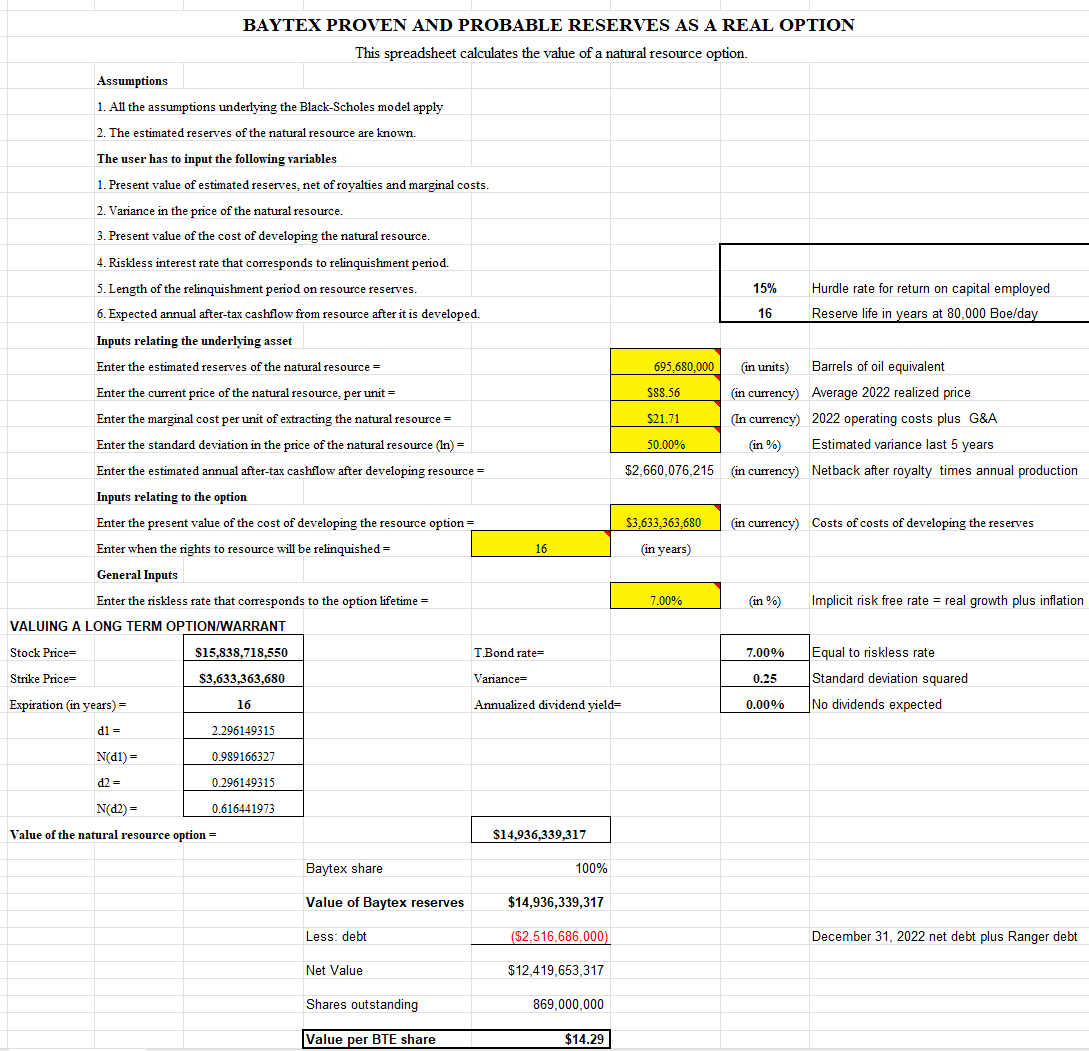

Baytex Energy (BTE.TO) is trading at CAD$4.33 a share today, well below intrinsic value. Resource companies are best valued using a modified Black-Scholes methodology that recognizes their reserves of proven and probable oil & gas are analagous to call options on future commodity prices. A stochastic method of valuation takes into account the volatility in commodity prices and avoids the typical valuation error of trying to forecast future prices, a virtual impossibility. Baytex is a high risk stock (as are all oil & gas explorers and producers) and I use a 15% after tax hurdle rate as an acceptable return to compensate for above market risk. Market averages have returned about 9-10% on investment for many decades and a 50% premium is adequate risk adjustment in my opinion.

Using Baytex’s 2022 year end date I calculate the option value of Baytex reserves as the equivalent of over CAD$14.00 a share. Here is that analysis.

At present, recession fears and the tail risk of the U.S. debt default have put energy names in the penalty box creating opportunity for the brave. I see little risk of Baytex failing as a company since its debt levels are now below annual cash flows and falling, although management can screw up anything with enough effort.

Based on the disclosures filed by Baytex and the limitations of the Black-Scholes model applied to valuation of oil & gas reserves, I see Baytex as deeply undervalued.

Speaking of Baytex a former head of BTE was on the Rosebros podcast yday

https://rosebros.ca/pages/podcast

Anthony Marino (Tenaz Energy)

Eric N on BNN May 30th talked up BTE, saying the Ranger acq will close in 3 weeks and the EagleFord is misunderstood. The existing operator is bad and they believe they can get a lot more out. If you recall EF oil is priced above WTI. He said they had 40m shares and had even bought 1m more before the show...