Baytex Energy is a speculative winner if oil prices remain firm

Think of Baytex common shares as a "real option" on its assets

Modern valuation methods recognize that the equity of heavily indebted companies can be seen as a “real option” on its assets with a strike price equal to the amount of third party debt and an option period equal to the duration of its debt. The Nobel prize winning work of the late Fischer Black, Myron Scholes and James Merton provide the powerful Black Scholes valuation model frequently associated with the valuation of stock options but recognized by valuation experts as having broader application of particular merit in the valuation of resource stocks.

Oil & gas and Mining stocks share important characteristics. Once a resource has been found the benefits of its exploitation are determined primarily by two factors beyond the control of the resource company operating the facilities exploiting the resource - the amount of the resource itself and its market price. Investment graveyards are rife with losses experiences by investors who chose companies with competent management and excellent energy or mining resources who fell victim to a collapse in commodity prices and excess use of debt by the particular company.

I have plenty of scar tissue from losses on such companies including Mercator Minerals, Labrador Iron Mines Holdings, Penn West Petroleum, Pengrowth Energy, and Lightstream Resources Ltd. After suffering those losses, I registered for and i 2019 completed the Advanced Valuation graduate program at New York University’s Stern School of Business under the leadership of world renowned valuation expert Aswath Damodaran. During that course, I became aware for the first time of the power of the Black Scholes model to value “real options” and not just stock options.

Professor Damodaran has written extensively about the valuation of the equity of highly indebted companies (even those whose debt exceeds the value of their assets) using Black Scholes. When oil prices fell in 2020, Baytex Energy was such a company. Oil prices have recovered but using Black Scholes to value Baytex equity remains worthwhile since the option valuation incorporates the volatility of commodity prices and provides a more reliable valuation than DCF or NPV which require the valuator to assume commodity prices, a tenuous assumption at best.

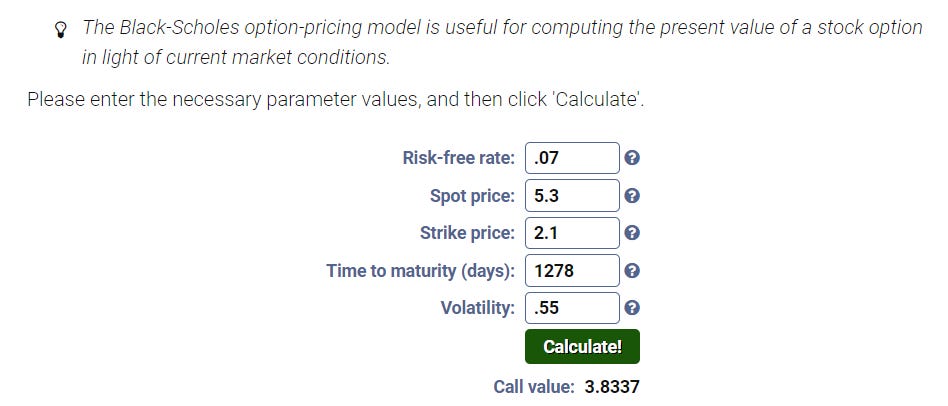

Baytex reports debt and third party liabilities of $3.2 million and at today’s market price has an Enterprise Value (market capitalization plus debt) of $5.3 billion. I estimate the volatility in the value of Baytex assets at 55%. The duration of Baytex debt is approximately 3.5 years. The implicit risk free rate of return (equal to real growth plus inflation) is approximately 7%. With these inputs, a Black Scholes valuation of Baytex common equity is straightforward and returns a value of $3.8 billion or $6.75 a share based on 570 million shares outstanding.

At a current market price of $3.75 a share, Baytex appears undervalued and the degree of undervalue is likely to rise if oil prices remain firm since the company is rapidly retiring debt.