Baytex Energy has become a safe bet on oil

Debt is now under control

It is not that long ago that Baytex Energy (BTE) barely avoided bankruptcy after buying Raging River through a share exchange in 2018 and diversifying its heavy oil base into very profitable light oil. The company’s $2.6 billion 2014 foray into Eagle Ford with the acquisition of Aurora Oil & Gas Limited added too much debt and exposed the company to insolvency risk. The Raging River acquisition stabilized the company somewhat but by year end 2018 debt still exceeded $2 billion.

The company had a rough ride. Shares traded close to $50 a share in 2014 but Baytex management feared dilution and bet the company on a hope that future commodity prices would be firm enough to carry the load. The result - the shares fell dramatically to hitting as low as CAD $0.30 in the spring of 2014. Baytex is a lesson in management hubris and financial mismanagement, but not one unique to Baytex. Penn West (now Obsidian, symbol OBE), Bellatrix, Lightstream Resources, Bonavista, and Pengrowth all made similarly terrible decisions in more or less the same timeframe. An apparent pandemic of stupidity infected the Petroleum Club in Calgary just a few years before the COVID pandemic appeared on the scene, a reminder to investors that projections based on monotonic growth in commodity prices lead to unhappy endings.

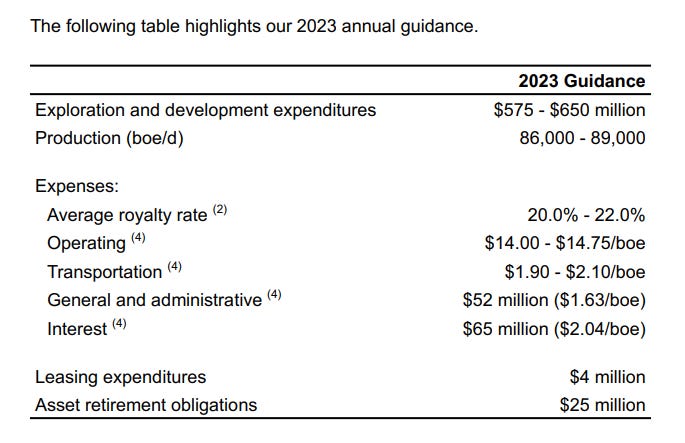

But management has now found religion and applied some discipline to both drilling and financial management, and debt today is less than CAD$1 billion and cash flow from operations is running north of CAD$1 billion, at least for 2022. The company has set a capital budget for 2023 of CAD$575 to $650 million and is on track to generated free cash flow of somewhere around CAD$500 million, further reducing debt.

Investors seem stuck in a time warp since with about 550 million shares issued and outstanding, the company’s market capitalization is ~CAD$3.3 billion and more or less unchanged since 2019 despite the considerable improvement in operating performance and debt reduction.

Baytex has some terrific acreage in the Peavine part of the Clearwater play and that relatively small asset is already throwing off tons of cash flow (about CAD$150 million) and growing very rapidly with well costs paid out in a few months rather than a few years. If management sticks to its last, eschews “buybacks” that may deplete cash and delay debt retirement on the eve of a recession, and continues to strengthen its balance sheet, market will recognize the value of its very fine assets and the share price could readily double or triple from here.

Famed fund manager Eric Nuttall is ebullient about the prospects for Baytex and sees a price of CAD$14 as in the cards. Nuttall promotes share buybacks but I prefer management to first get their company to a debt free state and then payout surplus cash flows as dividends. Nuttall gets paid based an assets under management and his views are biased by his own compensation, but investors don’t benefit from higher stock prices unless they sell to someone else and as a group don’t make out well. Investors do well from buying at low valuations and developing a portfolio that pays out dividends for years to come.

Notwithstanding that disagreement, I agree with Nuttall that Baytex is undervalued and investors who build a position today will profit.

Shrinking WCS differential to about $15 and the new U.S. listing a bonus bonanza!

Oops on the timing here...