Bank of Nova Scotia is worth banking on

Analysts ignore its earnings power and conservative risk profile

In its last earnings release, Scotiabank (BNS.TO) took larger provisions for credit losses than its peers, with a sizeable portion of the provision taken against loans that were in bank parlance “performing” meaning principal and interest continued to be paid when due. Scotiabank’s risk management culture has been a strength of this major Canadian bank for decades, earning a reputation for sensible approaches to risk dating back to the days when my friend Stephen Hart was Chief Risk Officer and my friend Peter Godsoe was CEO, if not longer. Stephen retired in 2017 but his legacy endures. A culture of sensible risk management positions a large bank to endure economic downturns, periods of volatile interest rates and the outgrowth of thoughtless Liberal economic policies (under Justin Trudeau) that threaten economic collapse in Canada if not soon bridled by a new government.

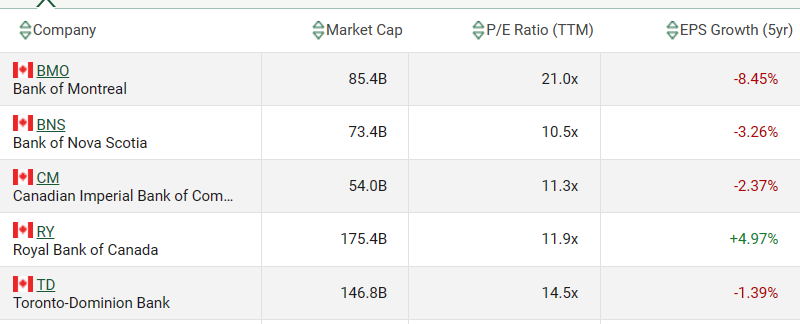

At CDN$60 per share (more or less) BNS stock has fallen from over CDN$90 per share in February 2022 and now trades close to book value and yields almost 7%. There has rarely been a better time to buy shares of Scotiabank than right now. Analysts hate it, preferring Royal Bank (RY) and Toronto Dominion Bank (TD) which trade at higher multiples of book value and lower yields reflecting investor interest is their higher returns on equity and the market assigning them higher price to earnings multiples (PE multiples). PE is a poor valuation metric for a bank, since it encourages bank management to manipulate provisions for credit losses (PCL’s) to smooth or even inflate reported earnings. A better metric for bank valuation is the simplicity of book value (BV). Unlike most public companies where BV can be misleading when legacy assets such as real estate or mining or oil & gas reserves contribution to BV do not reflect current or future cash flow potential, BV for a bank is little different from “cash” since banks assets and liabilities are all financial in nature with a tiny portion of the balance sheet comprising physical assets.

It is rare to be able to buy a Big Five Canadian bank at or below BV and historically investors who have taken the plunge to do so when such opportunities present have enjoyed double digit returns for decades thereafter. My first investment in Canadian bank shares was in the 1980’s when there was rumour Dome Petroleum (at that time a major Canadian oil company) might default on a billion dollar loan from CIBC (CM.TO) and Commerce shares fell to five times earnings and sported a 15 % dividend yield. I bought a few CM shares and never looked back.

Markets theoretically look forward but analysts typically look back, and base their recommendations on historical trends despite claiming “past performance is no guide to future results”. As a result, both analyis recommendations and so-called price “targets” for bank shares as well as current trading prices imply higher PE multiples for some banks and lower for BNS.

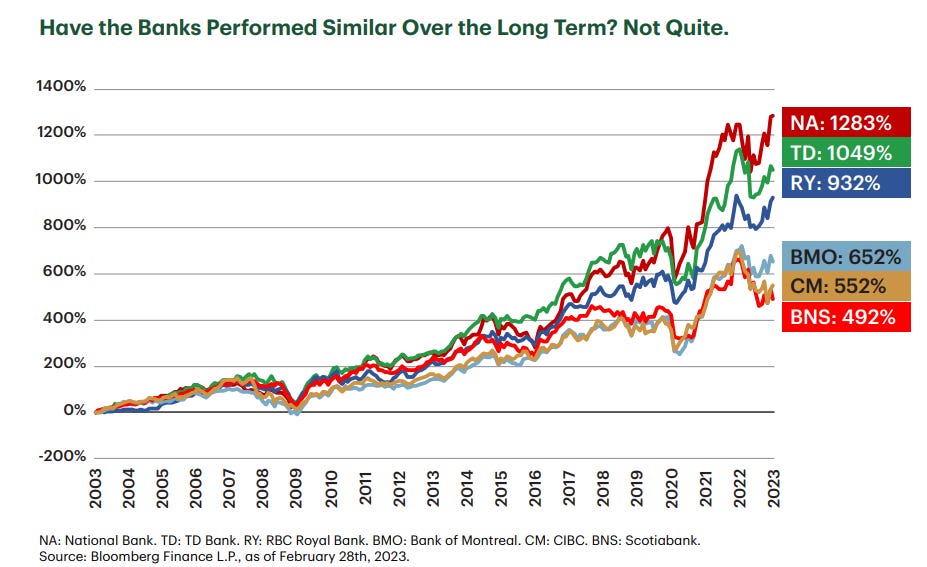

Looking back twenty years, from 2003 to 2015 major Canadian banks had similar “performance”, but higher multiples and trading prices of NA, TD, and RY had these banks running ahead of the pack from 2016 to date. The factors giving rise to that dichotomy are in common to the banks, so better management of credit risk, growth through acquisition and cost control have differentiated outcomes. My bullish thesis on BNS is like buying the worst house on a street of high end homes - longer term that strategy works well in real estate and in my opinion will work well in banking. I expect looking back ten years hence we will see a chart where BNS, CM and BMO “outperform” since the benefits of past performance are already in the share prices of NA, TD and RY and they are more vulnerable holdings.

I admit this is a contrarian view. No surprise, I have always been a contrarian. All kites fly in the same winds and the Canadian environment for banking will continue to favor the banking industry for longer term growth and dividend income. Buying the banks with the lowest price to BV ratio is more likely than not to outpace the returns on those where the benefits of their strategy and portfolio is already recognized in their share prices.

In another oddity of capital markets, call options on BNS shares at a CDN$50 strike price that don’t expire until January 2026 are trading with CDN$1 of their intrinsic value, about CDN$11 a share. I couldn’t resist so I purchases options on 5,000 BNS shares for about CDN$55,000 and expect to (a) either lose my investment if BNS shares fall in trading price to reach and stay below CDN$50 a share (a 16% drop from today) or enjoy a very large gain if BNS shares recover to reach their 2022 trading price of ~CDN$90 a share before my options expire in 2026 and I will realize CDN$40 per BNS share for my CDN$11 per share investment, over 300% in a two year period. Whatever the event, I expect my CDN$55,000 investment will mature with a value between nil and CDN$200,000 or so. It is this sort of lopsided outcome that has contributed to me becoming quite wealthy during my 52 year investment career, not without periods of substantial losses, I must add.

I like those odds and may add to my risky bet.