Ask why Eric Nuttall trades so much

Is it to improve returns or develop new clients?

Eric Nuttall has become famous among energy investors for his frequent appearances on BNN Bloomberg and his willingess to share his reasoned views on the outlook for energy stocks. There are few (if any) energy analysts with as large a following or who command the attention of investors to the same degree. He has earned his place in the investment community and earned the respect of many investors, me included.

But I question why he trades so often. Trading is not free and comes at the expense of commissions and transaction fees, and given the size of the NinePoint portfolio, has an effect on market prices both when NinePoint is buying or selling. I make it a point to listen to Eric whenever he appears on BNN Bloomberg to discuss energy stocks and keep track of his “top picks” which I presume are companies he suggests listeners buy and not those he is planning to sell in the short period after promoting them on BNN Bloomberg. I don’t think he has any agenda other than to earn more for his investors and for himself.

NinePoint Energy Fund management compensation includes performance bonuses as well as base fees. Many think this produces better “alignment” between Eric as manager and his clients, the ultimate investors. I have some concerns that incentive compensation for fund managers simply reduces returns to investors and encourages gambling, since once a bonus is earned it is not repaid if the investments later sour a bit. I stay away from any involvement in organizations where the compensation system appears to me to be inimical to my success as an investor. In the case of energy funds, stock prices typically rise in tandem with commodity prices and fund managers paid incentives are being paid for rising commodity prices over which they have no control and make no contribution whatsoever.

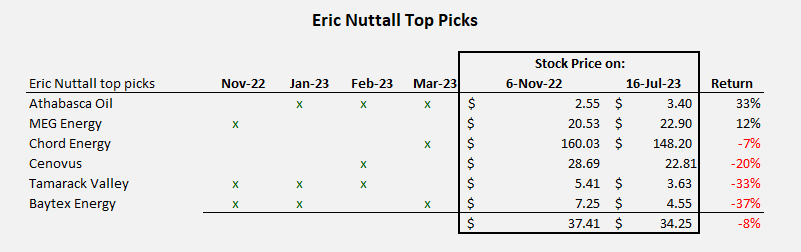

Eric’s “top picks” have on average lost 8% in 8 months. All of the companies chosen are solid, well-managed and with excellent assets and over the long term should be good investments. A loss of 8% in the past 8 months is likely a better performance than energy indices (I have not checked but it has not been a period of robust results from energy companies as both oil & gas prices have weakened during the period). But with respect for Eric, it is hard to see how the “churn” evident in the NinePoint portfolio benefited investors based on performance to July 16, 2023, the date I wrote the first draft of this article.

To counter any claim of “cherry picked” dates, here is Morningstar’s summary of Ninepoint’s performance for the past decade. A great performance in 2022 earned Ninepoint top fund ranking in Canada and a top percentile performance for the past decade as ranked by Morningstar, but the past year has been unexciting.

Eric Nuttall is a terrific analyst who does first class research on Canadian energy names and has an earned reputation for attention to detail. But he trades far too often and his fund has an MER of 1.8% which punishes his clients and a turnover rate of 207% - evidence of an inability to stick with good choices. I am reminded of Peter Lynch’s words to the effect that selling your winners and keeping your losers is like pulling up your flowers and watering the weeds.

As Warren Buffett has been quoted “The stock market is an efficient mechanism for transferring wealth to the patient from the impatient” or words to that effect. Active managers like Eric might impress more by being less active. Stock prices, cash flows and profits of energy companies are affected most by energy prices and the rise and fall in commodity prices affects all companies. Switching between solid names based on a mercurial view of what commodity prices might do in the coming months is in my opinion a fool’s game. It benefits brokers more than investors. If North American oil prices remain in the WTI $70 range or higher and Henry Hub natural gas trades between $2 and $4 a gigajoule as seasonal demand ebbs and flows, oil & gas companies will be fine. Eric is primarily an “oil bull” and rarely invests client money in natural gas stocks. All of the names in his recent list of “top picks” are primarly heavy oil producers and all will enjoy or suffer much the same experience as the price of heavy oil rises or falls. Picking six names affected by the same forces doesn’t really qualify as “diversification” to the extent that has any value.

I am big fan of Nuttall’s and admire his work. He would do even better if he calmed down, stopped touting the claim that any given E&P could go private in x years based on their free cash flow for a reporting period, and simply buy well-run names when they are out of favor and hold them for complete cycles if not longer. His emphasis on “buybacks” is destructive to his fund, since the money goes to others and his clients don’t get any of it, instead being treated to another round of wishful thinking that commodity prices will improve and the energy names are “undervalued” and could go private in a few years based on free cash flow and should keep buying back more stock.

Every investors should ask themselves if they have the expertise to formally evaluate the worth of a business and how much risk exists that their theory on commodity prices is wrong. If they don’t they rely on Nuttall and his ilk and Nuttall is rarely bearish on energy despite the cyclicality of the energy market. His frenetic trading evidences a lack of confidence that inactivity would be seen as wise by his clients, yet history shows inactivity and patience produce the best results. Buy well - hold. It worked for Warren Buffett and the late Charlie Munger and will work for you too.

Great advice!

Tmx is one solid reason to hold heavy oils in canada, no?

An additional $10 gain in oil prices revenue when WCS is strength into single digit difference for good.