Are investment advisors parasites?

Few of them beat the market but they all charge fees for trying

The plethora of advertisements soliciting customers for investment advisory or “wealth management” firms seems to have hit a fever pitch since COVID-19 saw most people staying home glued to screens to break the boredom of senseless lockdowns mandated by governments who pretend they are “saving lives” when they are actually restricting personal freedoms for political advantage. Certainly some level of government action was and is necessary to prevent this pandemic from spiraling into a repeat of the 1919 Spanish flu pandemic which infected one third of the world’s population and killed some 50 million people. It is an interesting aside that the 1919 pandemic ran its course in a little over 2 years without worldwide vaccination campaigns or widespread lockdowns.

Most individual investors know little about markets and need help to find investments to save for their retirement or simply put away some money to save up for a down payment on a home or buy a new car. That opens the door to the cottage industry of financial professionals who seem to have no problem with home ownership or car purchases with many of them living in Forest Hill and driving late model BMW’s or Range Rovers. Nine out of ten of the largest “wealth management” firms underperformed the stock market over the past fifteen years and that relative performance seems to be deteriorating rather than improving.

Most of the fund managers have professional certification, a legal necessity for managing public money for anyone but “qualified investors” which is a legal term for people rich enough to be prey to even less competent advisors and unworthy of public protection. Those professional certificates are often backed by accounting designations, MBA’s and courses from various financial institutions. What they seem to lack is any basic understanding of what comprises risk and what comprises value, often reducing the worth of a stock to hackneyed but age-old metrics like Price to Earnings ratios; Enterprise Value to Earnings Before Interest Taxes Depreciation and Amortization (EBITDA). That makes it simple for them to claim that a company with a lower such ratio is likely a better investment than one with a higher ratio, or to claim that a higher ratio is warranted for any particular company owing to expectations of higher growth or some impending technology breakthrough. And, to some extent they are correct.

But if they are correct more often than not one might expect that to manifest itself in returns greater than market averages which investors can approximate by putting their money solely in Exchange Traded Funds tied to the major indexes, where “management fees” are miniscule and the investor is more or less guaranteed a return close to the return on the market as a whole. But it doesn’t. Few advisory firms outperform the market in any given year and the majority underperform with their clients not only experiencing sub-market returns but also contributing to the rewarding lifestyle of the advisor who gets the fee regardless of the results in most cases, and where the advisor is lucky enough to see superior returns in a year (more often than not the random outcome of chance) the advisor frequently charges a premium or bonus.

Advisory firms exist because there is a need and because they peddle the view that it is possible to systematically outperform the stock market. And, they are right but they are incapable of doing so because in general they lack the understanding of how to do so having failed to study the Nobel Prize winning works of Eugene Fama, Richard Thaler, or Robert Schiller who have demonstrated the possibility of doing so.

In the history of fund management, I have only made the acquaintance of one fund manager whose performance routinely beat the market by a wide margin - Peter Lynch. His now famous Magellan Fund earned an average rate of return close to 29% over its 14 year life. I have the pleasure of meeting Peter while President of The Enfield Corporation Limited (“Enfield”), a company I founded in April 1984 which grew in 5 years from an initial employment of about 240 people to about 9,000 people in 1989 when Enfield was taken over and I was removed as CEO. In the 5 years I was CEO the company was not only profitable every year but also earned a peak profit of over $60 million in the fiscal year ended June 30, 1987. Helix Investments Limited purchased 100,000 shares or 25% of the founding equity for $100,000 and three years later sold that position for north of $40 million. Under the ownership of an entity controlled by what is now known as Brookfield Asset Management, Enfield was stripped of its assets and languished with massive losses for its investors, including me.

Eugene Fama and William French advanced valuation theory beyond the Capital Asset Pricing Model (“CAPM”) that had been popular for years with a three-factor model that recognized that over longer periods two classes of stocks outperformed the markets averages - those with relatively small market capitalizations and those with high book value to market price ratios. If there is an advisory firm that has the discipline to build its client portfolio using the Fama-French model, I can’t find it.

Richard Thaler, a behavioral economist, advanced work initially done by Daniel Kahneman and the late Amos Tversky who discovered that graduate students would give diametrically opposite answers to the same questions if they questions were framed differently, apply this odd behaviour to investment decisions. Thaler discovered that investors over-reacted to bad news and under-appreciated positive developments and theorized that a portfolio comprising the bottom third of stocks from the Standard and Poor’s index (with minor modifications) held for at least a few years tended to outperform the S&P index by several hundred basis points over any extended period of time.

In his 2016 paper, Larry Swedroe applied the logic published by Thaler and Werner De Bondt in 1985 to data from 1927 to 2015 finding that there were period where the “equity risk premium” or the returns on stocks compared to the returns on low risk bonds diverged from any value that conformed to economic theories or common sense. His finding tended to confirm the over reaction to risk Thaler and De Bondt had identified. Couple that with the reality that advisors need to trade stocks (rather than simply hold them) to persuade their clients they are actively managing their portfolios and the stage is set for lower returns and higher advisory fees.

Robert Shiller, another Nobel laureate, created the cyclically adjusted price earnings multiple (CAPE) metric to give some indication as to when stock markets are over-valued or undervalued. Shiller seems to suggest that investing when CAPE multiples are low and reducing exposure to stock when they are high will produce greater returns and, in my opinion, he is almost certainly right. Professor Shiller has won some fame for his work comparing real estate prices to construction costs and broadly predicting housing risks with some success. Shiller currently sees risks of “bubbles” in housing, stocks and cryptocurrencies. In my view the mania over cryptocurrencies is unlikely to have a happy ending since these are not currencies, have no sovereign backing, and offer less secure transactions than mechanisms such as Interac, Visa or Mastercard despite their “blockchain” underpinning since purchase of crypto requires an insecure opening transaction through one of the proliferation of “exchanges” (several of which have failed leaving investors holding the bag for billions of dollars in losses) and exiting the product requires another equally insecure transaction.

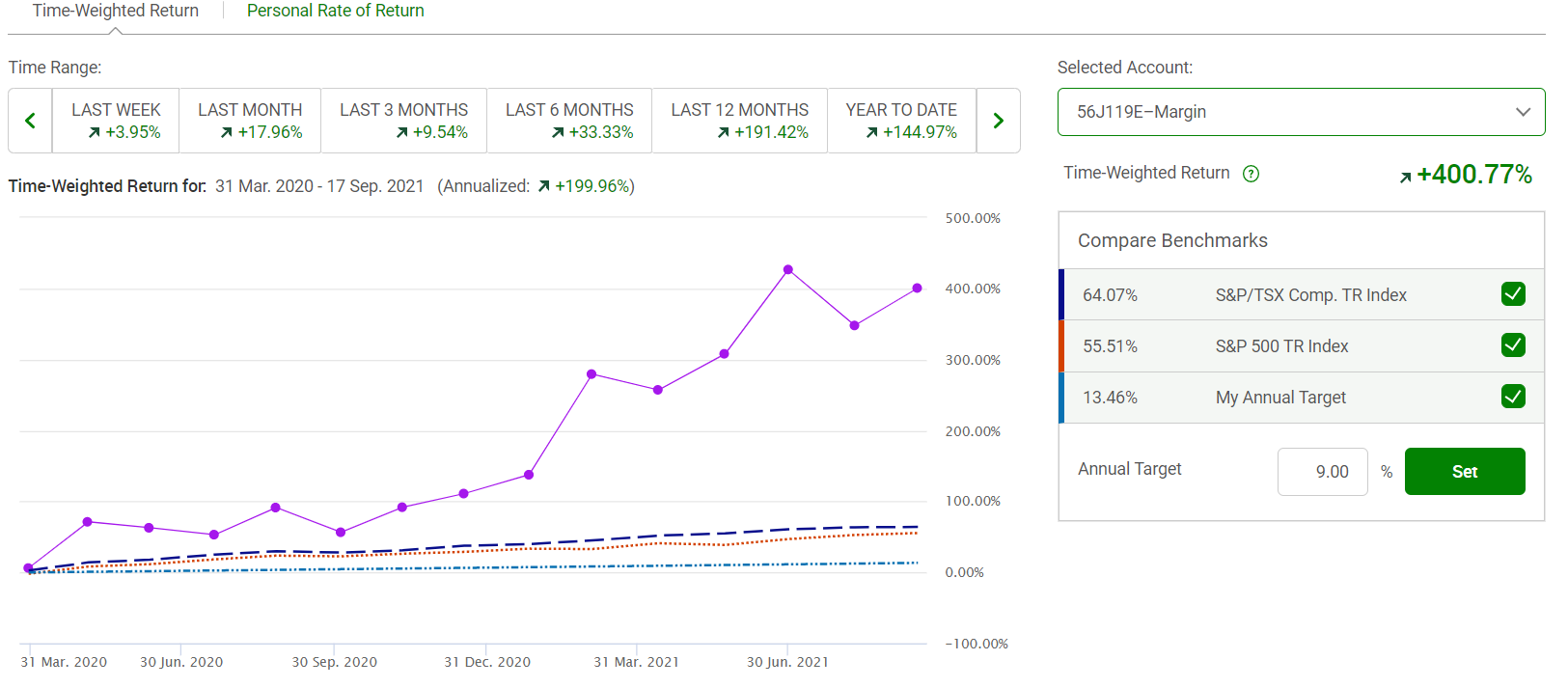

Aswath Damodaran, who teaches Advanced Valuation at New York University’s Stern School of Business, is a world renowned valuation expert. I invested a few thousand dollars in tuition fees to take his course in 2019, and began to apply valuation theory to my investment decisions. The results have been positive, with returns since March 2020 of over 400% beating market indices by a substantial margin.

I don’t recommend individual investors lacking formal education in valuation and markets attempt to duplicate these results but do suggest they eschew “advisors” in favor of index funds and decide whether to alter their mix of cash and exposure to market risk based on a review of the Schiller CAPE index. No one can predict markets but prudence dictates holding more cash and taking less risk when CAPE multiples are high and the opposite when they are low.

One of Canada’s best performing funds is the Ninepoint Energy Series F fund managed by Eric Nuttall which boasts a one year return of 168% and has a management expense ratio of 2.12%. The 168% looks attractive but pales in comparison to the 191% return I have enjoyed managing my own money over the past 12 months, and this fund’s 10-year performance amounts to an average loss of 2.09% a year, about equal to its management fees. That may work well for Eric but it doesn’t work for me.

We all need savings to endure the ups and downs of live events and we all should have money set aside for retirement. The safest way is to avoid advisors and “managed money” and use your TFSA and RRSP to hold well-diversified passive funds or index funds with low management expense ratios, and keep a reasonable cash reserve. Markets go down as well as up. You can’t avoid the industry I have described as parasitical but you can reduce the degree to which it eats you alive.

I am going to write an article every few weeks on specific stocks that are undervalued based on modern valuation theory. They may remain undervalued for extended periods of time and there is no assurance the market will ever price them at their intrinsic value, but the likelihood they will outperform the market is high. This information is free, but remember that free advice is often worth what you pay for it.