ARC Resources has great assets

But Birchcliff Energy is better value for money

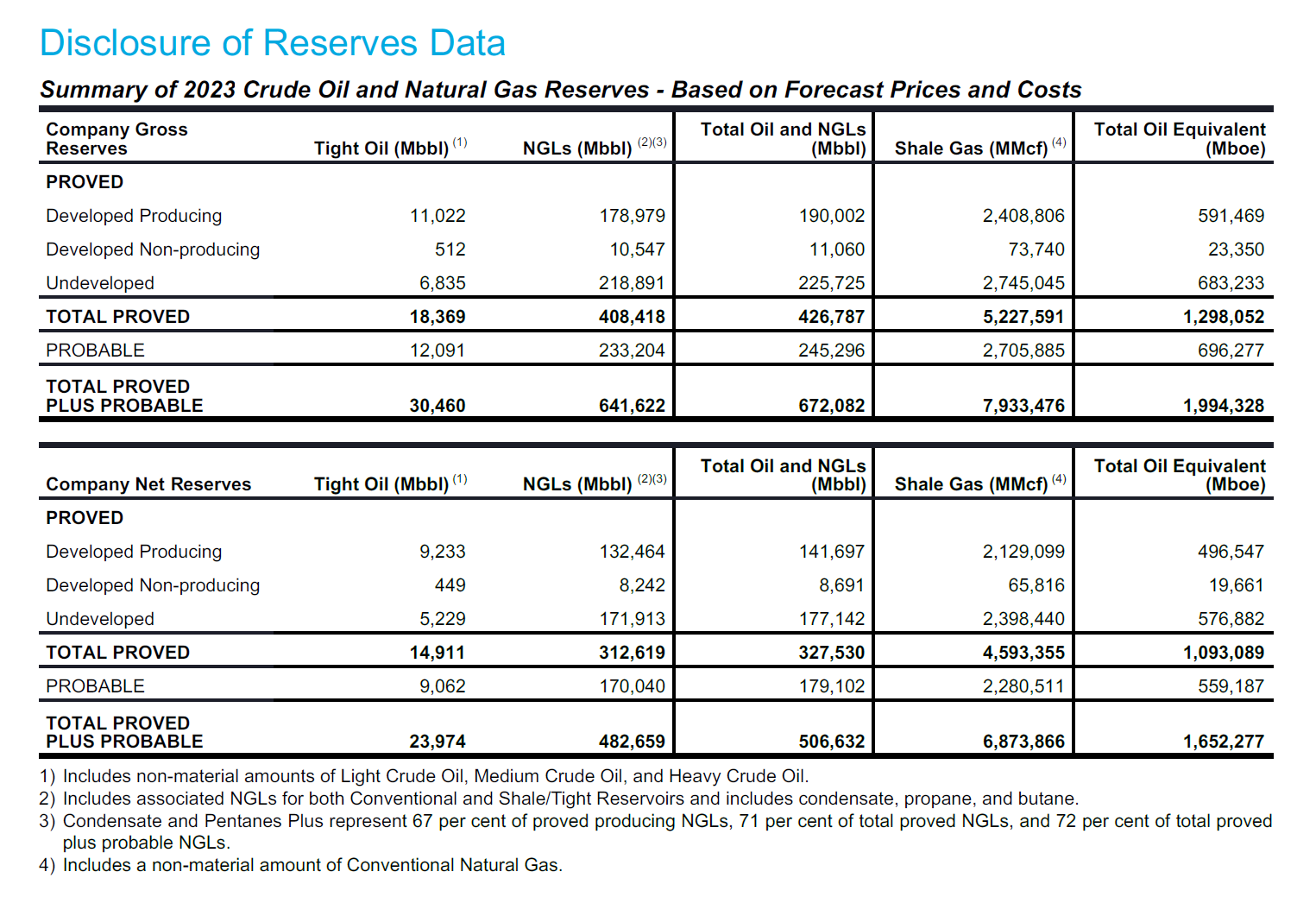

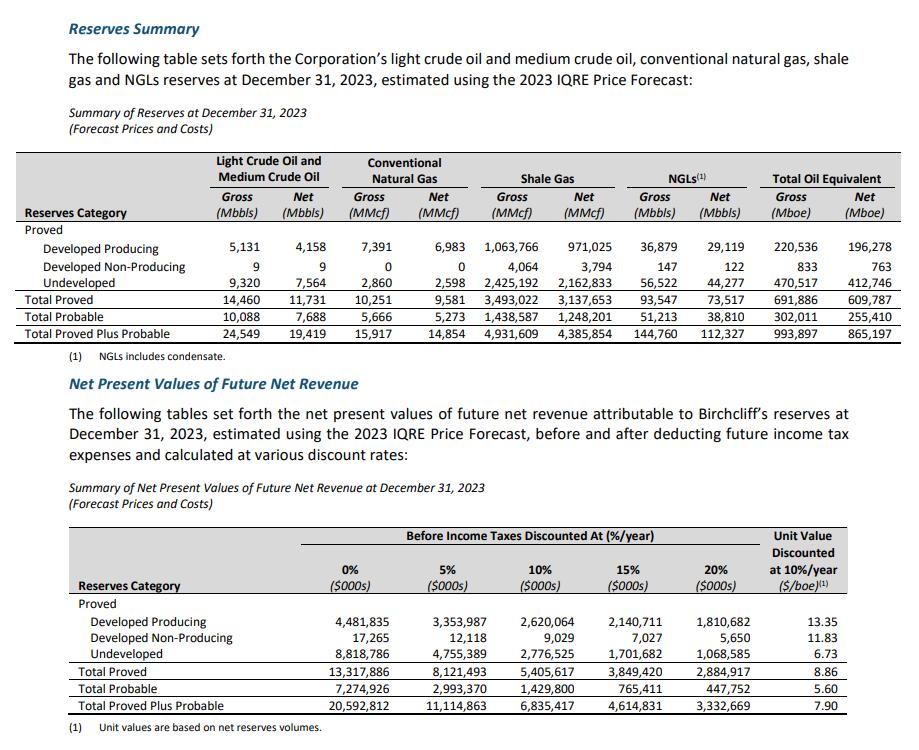

ARC Resources (ARX.TO) annual information form (AIF) seems to be a rare read for many energy investors who apparently confine their due diligence to the company’s corporate presentation, quarterly and annual reports with their accompanying Management Discussion & Analysis (MD&A) and analyst’s reports. Few refer to the NI 53-101 reserve report which is the best source of information on the energy assets of the company. ARC has some of the best assets in the Western Canadian Sedimentary Basin (WCSB) with total reserves of 1.6 billion barrels of oil equivalent (BOE).

Without further exploration successes, and with annual production running around 330,000 BOE/day or ~120 million BOE a year, ARC has some 13 years of reserves assuming development of the undeveloped reserves and realization of the probably reserves.

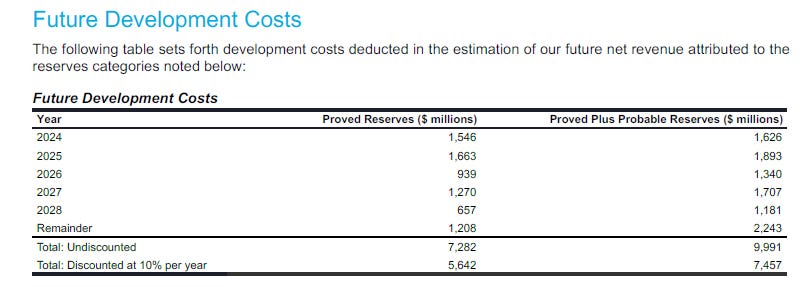

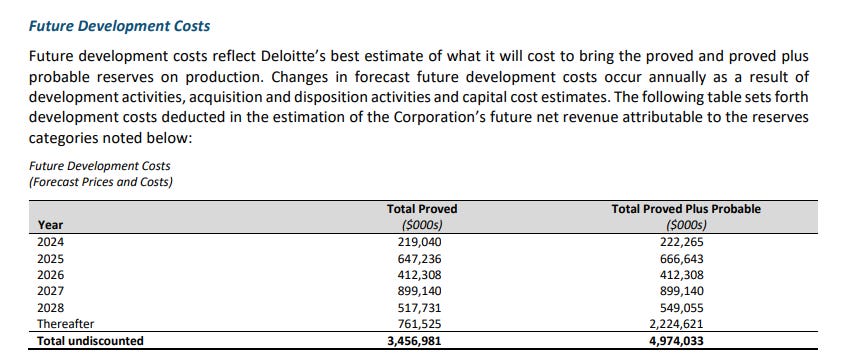

Future development costs (FDC) comprise an estimated $10 billion.

ARC benefits from a high liquids content in its natural gas with condensate and pentanes comprising 72% of the 506 million reserves of natural gas liquids (NGL’s). Those liquids attract prices similar to and often at a premium to the price of oil.

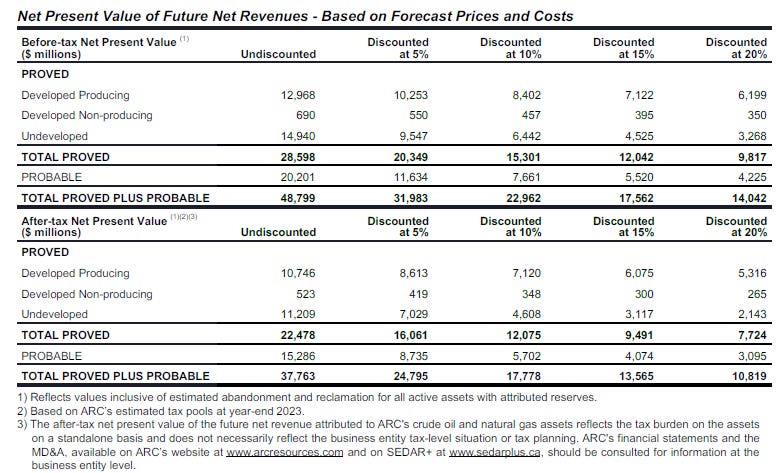

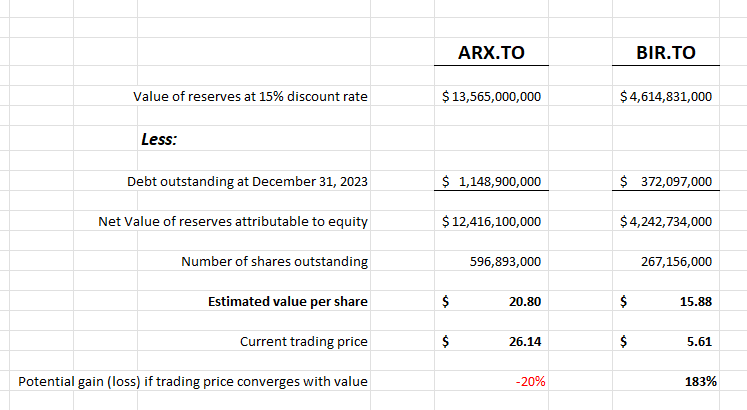

The present value to be realized by exploiting those reserves amounts to about $13.5 billion at a 15% discount rate.

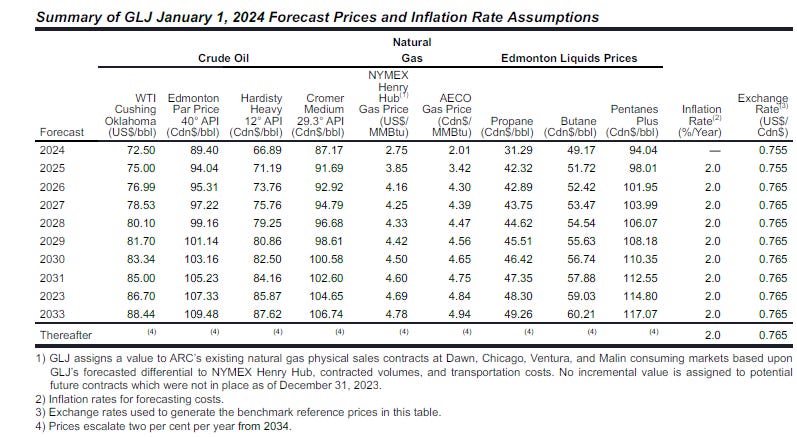

That value results from assumptions that oil & gas prices will remain at levels at or above current prices. Here are those price assumptons:

History has shown that forecasts of commodity prices are typically unreliable and a forecast of monotonically increasing prices with cost inflation at a flat 2% per year is tenuous at best, but is the best available information in the eyes of the independent reserve valuator (in this case GLJ). So if that forecast were reliable, investors could buy ARX.TO shares at today’s price of about CDN$27 and take a holiday while their passive investment earned them a significantly better return on investment than energy investors have enjoyed in any 10-year period in recorded history. That seems unlikely, but the discipline of using independent reserve reports and hard data to compare companies is in my opinion preferable to opinions or promotional speeches by self-interested managers.

I often compare ARC Resources to Birchcliff Energy (BIR.TO), another Canadian natural gas based company, albeit smaller in size and scale than ARC. Birchcliff reserves comprise and estimate 865 million BOE, a bit more than half those of ARC, and have an estimated value of $4.6 billion based on a 15% after tax discount rate similar to that used for ARC.

Birchcliff FDC’s amount to about $5 billion.

To compare Birchcliff and ARC, two factors need to be considered: Debt and the number of issues and outstanding shares. With reserve values adjusted to a per share after debt amount, and compared to current trading prices, an investor can create an apples-to-apples comparison of the value of these companies and their respective shares.

So let’s do that:

ARC is a very popular stock, and investors have enjoyed watching it acquire Seven Generations and start to expand in the liquids rich Montney cutting some terrific deals to gain exposure to markets outside of Canada including liquified natural gas (LNG) contracts. The company has an enormous asset base and ranks as one of the largest natural gas producers in Canada. ARC management thinks it prudent to “hedge” against a potential price drop and to direct money to buying back stock in preference to either developing its asset base or paying dividends. ARC lost about $2 billion on hedges in the past few years, but is undeterred on its hedging program.

Birchcliff is an unpopular stock, and investors lament the fact that Birchcliff management have elected to curb growth in a low natural gas price environment and pay more dividends than are covered by current free cash flows. While smaller, the company’s asset base is not inconsequential and management of Birchcliff have decided to offer shareholders an “unhedged” exposure to future commodity prices. Birchcliff limits its share repurchased to those made to offset share based compensation, keeping its share count more or less constant.

I approach investment without emotion based on an objective analysis of the investee company which I approach with complete detachment. I did own ARX.TO shares and sold them in 2022 for a gain of $164,000 when I became dissatisfied with ARC Resources management. I have not owned any shares of ARC since that time.

I do own 170,000 shares of Birchcliff and will keep them as a long term investment. I am satisfied that Birchcliff management is competent, unwavering in its commitment to provide shareholders with an unhedged exposure to natural gas prices, and excellent stewards of the assets under their stewardship.

As most readers know, I use the data from the NI 53-101 reserve reports to populate entries into a modified Black Scholes valuation model that makes no assumption about future commodity prices but assumes those prices are log-normally distributed with a standard deviation close to the volatility of the underlying commodity. Based on those valuations, I have estimated that Birchcliff shares have an intrinsic value of $13.00 per share and ARC shares have an intrinsic value of $23.00 per share.

On each anniversay of this article I will provide readers with an update on the relative economic performance of ARC and Birchcliff and whether my judgment was sound or in the alternative whether I missed opportunity.

I do own BIR.to, which has been my most sluggish holding, but was surprised to see yesterday that National Bank revised their ARX target from 25 to 33 cad. https://twitter.com/emmpeethree/status/1781350140001046965/photo/1

We have similar investment styles. I truly appreciate all the extra information you freely give. I have both ARC for the dividends and hopefully some growth and BIR for the dividends and far more growth. I know some the management at BIR personally and they are absolutely the best in the business. I wouldn't consider selling unless some macro disaster forced me out of all of them. I also have TOU and PNE for gas and some Cdn oil producers. My investing focus is oil gas and nuclear since they are the basis of modern society and gold and silver because I think western governments are obliterating personal wealth and that is the only investment that I think will hold up to the destruction they create. Thanks again for all the information you give out.