And the walls came tumbling down . . .

Silicon Valley Bank's problems point to larger problems, far from over

People like to explain unexpected outcomes in language that is consistent with the world they way they want it to be, not with the way it is. Silicon Valley Bank (SVB) failed because its assets were long term treasuries and mortgage back securities with high credit worthiness but low liquidity and they couldn’t meet depositors demands to withdraw deposits when there was a “run on the bank”. Great story. But it doesn’t explain why the depositors were panicking about SVB’s assets since the “hold to maturity” portfolio comprised AAA credits.

No one is even trying to explain why the depositors panicked. The story that the “mark to market” on the long duration fixed income assets had wiped out SVB’s equity just doesn’t hold water. The only thing that forced SVB to sell assets from its “hold to maturity” portfolio was the rush to withdraw deposits and had that not occurred, all would have been just fine. Or would it?

With the market focused on SVB, Janet Yellen and Jerome Powell saw a different picture and that was a lot worse than failure of a bank that had mostly uninsured deposits and a depositor base that was spooked by something. What they saw was the “elephant in the room” - with the Fed raising rates, no one wanted to hold U.S. treasuries - not banks, not the public, not foreign investors, not institutional investors, and not me for certain.

The “contagion” did not take long to spread to Signature Bank and its immediate failure was attributed to its involvement in “crypto” but that story doesn’t hang together either. Signature simply loaned money and provided services to businesses involved in the “crypto” game and had good systems to control risk and manage credit as far as I can tell. As toxic as “crypto” is, I don’t think Signature’s involvement threatened the bank’s liquidity and the outflow of deposits was more contagion than a banking issue. In my opinion Signature was closed because the regulators thought it was a good message to the world that regulatory action could be relied on if there was any threat to depositors.

That narrative didn’t stop an outflow of deposits from other regional banks like Republic Bank. The Biden Administration immediately blamed the whole mess on Donald Trump (why not? they blame every other policy failure on Trump including the mess on the Southern border or the massive federal debt and huge deficits). There is something else going on and the evidence is profound and astounding.

That “something else” is that no one wants to buy U.S. bonds or even to hold them either directly or indirectly through the banking system. Incapable of finding other places to earn a spread over deposit interest banks balance sheet filled up with longer duration treasuries and mortgage backed securities. That game became toxic when profligate government spending, persistent deficits and a deepening shortage of fossil fuels drove inflation north causing the Fed to raise rates and the trading price of those long duration treasuries to fall. In short order, government bonds became a hot potato and no one wanted to own them.

How do I know? The answer is the swift and massive reverse of Quantitative Tightening with the assets held by the Fed suddenly rising by a staggering ~$300 billion in one week, unwinding months of QT.

About $165 billion of that rise was banks rushing to the discount window ($153 billion) and the new Bank Term Funding Program ($12 billion) established only last Sunday (reported by Bloomberg). The remaining $135 billion can only be the Fed open market purchases when it was supposed to be selling bonds as part of its QT program.

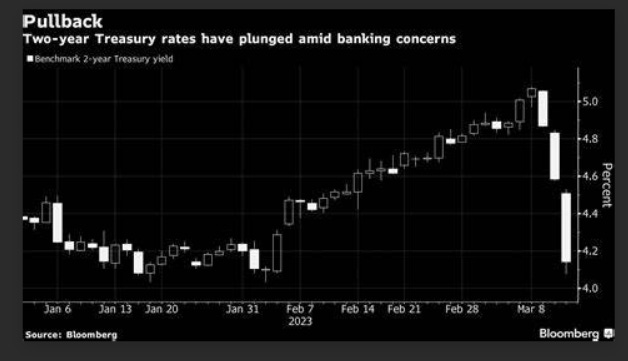

The remarkable 80 basis point drop in 2-year treasury yields three days was as much a result of direct purchases by the Fed as a “flight to safety”.

Banks had turned to the Fed for support when depositors started to withdraw their deposits and the Fed acted quickly to try and calm the nerves of depositors. At the same time, Treasury Secretary Janet Yellen assured SVB depositors they would get 100% of their money quickly even if it was not insured. This is an extreme move, putting the Federal government as the guarantor of bank deposits for every bank in every circumstance if taken to its logical conclusion. At the same time, Yellen or Powell or both of them urged money center banks to support Republic Bank and they agreed to a 120-day bailout package of loans to Republic of some $35 billion. What happens in four months is anyone’s guess but it is unlikely to be good.

This all started as a result of a $16 billion “mark to market” gap at SVB who doesn’t “mark to market” its “hold to maturity” assets. Ask yourself why it takes $300 billion of Fed lending and $35 billion of support from money center banks to contain a $16 billion valuation gap at SVB? Then ask why Credit Suisse, experiencing its own set of problems in a rising rate environment, needed a 50 billion Euro bailout earlier this week. The banking system problems are not confined to Norht America by any means and reassuring words from Christine Lagarde and European banking experts are far from reassuring. The 50-basis point rise in European rates in the midst of the chaos of the last week is evidence that Lagarde sees inflation as the greater risk and points to even higher rates that will exacerbate the tumbling value of sovereign debt in all markets.

I have long predicted that left wing governments would eventually borrow so much money there would be a “buyers’ strike” and that strike would be caused by rising rates to combat inflation, itself an outgrowth of absolutely stupid “climate policies” that pretend CO2 can cause global warming for political gain. Energy costs are central to every aspect of the economy and the resulting shortage of fossil fuels almost crippled the European economy (but for a warm winter). Rising rates have slowed the pace of economic growth and most economists think will cause recession which in the short term reduces both oil & gas prices and consumer demand hopefully by enough to bring inflation under control. Under control for how long?

Not long. A recession, high rates and continued climate nonsense will not add one barrel to fossil fuel output and will pretty well ensure the global energy shortage will deepen. Fossil fuel prices likely rebound quickly in any post-recession expansion. As they do, inflation will accelerate.

The recent dramatic rise in the Fed’s balance sheet pretty well assures the world that inflation will be around and stay higher for longer. Neither Joe Biden nor Justin Trudeau nor Rishi Sunak seem to have a clue about how their leftist policies (Sunak is a socialist pretending to be a conservative) will damage the world economy and keep doubling down on ideology (a synonym for stupidity in any leader) enacting or trying to enact higher taxes and more incentives to move to a “just transition” away from fossil fuels with zero chance that is even remotely possible or that it will make an iota of difference to world climate trends. Unfortunately for them, climate trends are unrelated to CO2 levels which have long since passed the “saturation” point and no longer have any ability to “trap” more outgoing long wave infrared radiation (LWIR) than they do today (a reality well set out in a recent paper by Dieter Schildknecht).

I believe the aggressive actions by Yellen and Powell are a tacit recognition that a global financial crisis is a serious threat and may turn out to be a band aid solution to a cerebral hemorrhage. Inflation is more likely to rise than fall in my opinion, for the most part because high inflation (an effective tax on the poorest in society) may be the only way to balance government debt servicing costs with tax revenues and resolve the sovereign debt burden’s now facing virtually every Western democracy.

Expect more “reassuring words” from central bankers, political leaders and Wall Street pundits. Don’t be reassured too quickly. Minor problems don’t need hundreds of billions in unplanned intervention by central bankers. Serious issues exist and won’t go away overnight.

The outlook is ugly. On the bright side, as my late father used to say “Cheer up. It will get worse”.

I recommend to listen to this great interview: https://open.spotify.com/show/4YWyPCna1Sg50fmRJGF0LV

Liquidity is a very complicated, subject and books like The Big Short will be written about this.

One thing to keep an eye on is: did the regulators really screw up by not forcing the banks to “mark to market“?

Instead, is it accurate to say the banks simply had to footnote the “mark to market” position? Which is not the same as processing the loss through their income statements.