Analysts love Advantage Energy

But the numbers just don't work for me

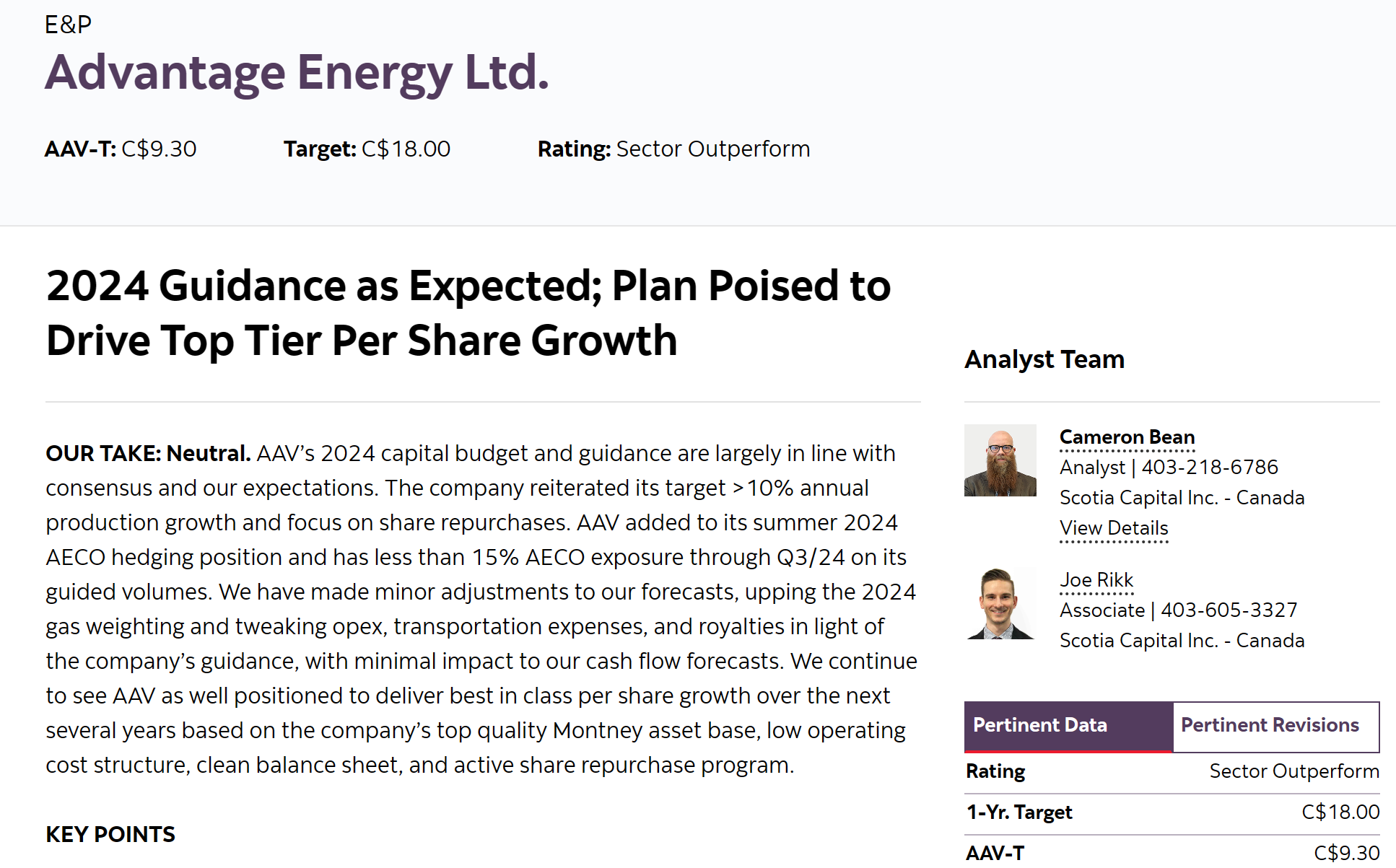

Scotia iTrade published an analyst’s report by Cameron Bean this morning, suggesting Advantage Energy (AAV.TO) might trade as high as CDN$18 next year, almost double today’s trading price.

No disrespect to Mr. Bean who is entitled to his opinion, but the numbers don’t support the valuation in my opinion.

Advantage is projected to produce annual production between 65,000 and 68,000 boe/day, 89% of which is natural gas. The company expects royalties in the 7-9% range, CDN$3.85 operating costs, CDN$3.95 transportation costs, and G&A costs of CDN$1.90 per boe or about CDN$47 million.

Advantage has a sizeable hedge book which protects a portion of output at about CDN$3.40 per gigajoule on average, and is exposed to AECO prices for its non-hedged output. Advantages liquids output is divided more or less equally between C5’s and NGL for which Advantage received CDN$77 per boe year to date 2023 and an operating netback of about CDN$17.00 per boe so far this year, less about $1.90 per boe for SG&A.

I like to use basic arithmetic to arrive at a “first blush” valuation. For AAV shares, I see operating cash flow of 68,000 x 365 x $15.10 = ~CDN$375,000,000 of pre-tax cash flow from operations, valued at 4x EBITDA gives an enterprise value of CDN$1.5 billion. Knock off about CDN$200 million of net debt, and the CDN$1.3 billion equity value is worth about CDN$7.50 for each of the 172 million shares outstanding. The company should have ~$100 million free cash flow and says it will direct those funds to “buybacks”. Buying back shares trading at over CDN$9.00 a share when they have an underlying value in the CDN$7.50 range won’t enhance value for shareholders.

Mr. Bean’s “target price” implies a valuation multiple north of 6 times EBITDA and is grounded on hopes for growth in production and cash flows. AECO prices today (the default for the non-hedged output) are in the CDN$2.40 range. A warm winter may see even lower prices.

In summary, and without a lot of formality or detailed analysis, I decided to short AAV shares. I am long Peyto, Birchcliff and Spartan Delta and if I am wrong about AAV I will be pleasantly surprises by the strength in my other natural gas holdings, and if I am right about AAV I can use the gains on the short book to add to my holdings of companies that don’t squander shareholder money on “buybacks” based on management’s desire for higher short term stock option gains, often the motive for “buybacks”.

Bravo!

Buybacks reward sellers, while dividends reward owners and encourages buyer of productive businesses.

You don't have to look much further than that... but to do buybacks at a premium to fair value is a breach of fiduciary duty.

Because of the vagaries of valuation "truth", buybacks are only justified by purchases at a substantial discount to low-end valuation.

BIR and PEY are two of my core positions. I did very well with SDE this year and kept a small position. With the selloff of the last month I've increased my position in SDE substantially. Time will tell if they can execute but the management team treated me well so well worth the risk. Birchcliff and Peyto were the same a few years ago and paid off in spades. I like AAV but they have that oil extraction technology under development and unless they can scale it I'm not interested.